It may be the summer doldrums but this issue of the Fortnightly is overflowing with worthwhile ideas. Pass it along to others and if you haven’t subscribed you can sign up here. Always free (and your email won’t be used in any other way).

If you missed it, in a recent posting we mused about those one-pagers so common in the investment universe.

The illusion of readiness

Inside the Mind of Mojo has only been available on Substack for a few weeks and the anonymous “Mojo” has already produced a number of great essays. The latest one, “The Illusion of Readiness,” is a must read.

At a time when pod shops are viewed as the repository of the best talent, Mojo identifies a problem in the pipeline:

The pod system has created a generation of analysts who mistake opportunity for readiness. I understand the analysts who prematurely sprint to be in control of their portfolio before they have earned it, but think, even believe, they have earned it. The whole ecosystem has been designed to reward short-term output, not building intermediate term and long-term foundation.

Instead of learning their craft and expanding their horizons, analysts are running fast down a narrow chute:

It’s because the ecosystem taught them to optimize for attribution, not absorption. Learning takes a backseat to optics.

Analyst pod theater. But it’s not entirely the analysts’ fault. Let’s be real. The ecosystem encourages all of this.

The piece is the kind of cultural tableau that you rarely find in investment writing, full of insights not only applicable to pod shops but other kinds of organizations too. For example, this describes a persistent problem in hiring within the industry — that individuals are given undue credit for results that relied upon the efforts of others:

And here’s the dirty secret about that early success: much of it isn’t even yours. The TMT analyst walks out with his entire AI playbook, charts and KPIs and the whole domino effect mapped out, none of which he actually developed.

Many employee selection mistakes (and manager selection mistakes) stem from such misattribution.

There’s much more to recommend, including the way in which Mojo uses Kobe Byant’s rules of improvement to contrast with the ethos that the pod shop model perpetuates.

Language barriers

Joe Wiggins highlights an overlooked yet critical fact for investors:

One of the (many) unusual features of the investment world is that it brings people together who are engaged in entirely distinct endeavours and assumes that they are (pretty much) doing the same thing.

He points out that individual investors can be susceptible to every new opinion that comes along because they lack a grounding philosophy. But language barriers “are also a major issue for investment teams”:

Teams with conflicting incentives and principles are inevitably beset by constant friction, frustration and disharmony.

In short, they aren’t talking the same language. (That’s why good due diligence work is attuned to the unique language of an organization and that used by different individuals within it.)

Language barriers act as impediments in a number of other ways too. Firms that manage money across a range of asset categories often fail to take advantage of their breadth of knowledge (which should offer actionable insights) because of the struggle to communicate across categories. Investment committees made up of disparate specialists often suffer from the same problem — the separate spheres of experience of the members can divide the group rather than unite it in a common purpose.

Foie Gras

With the title of his latest Basis Pointing posting, Jeffrey Ptak paints an indelible image that goes with the famous market adage, “When the ducks are quacking, feed them.” That saying is all about filling customer demands for a hot product without regard to whether it’s in their best interest to purchase it or not.

Ptak admits his leeriness about the current rush to include private assets in defined contribution plans (which is the main focus of product providers now that fewer institutions seem to be quacking for privates and some even appear to be choking on them).

But his specific concern is the inclusion of private allocations in target-date funds, since they are widely used as the default option for employees who are auto-enrolled into a plan. Are the assumptions used by managers self-serving? What are the operational and investment ramifications across a range of scenarios? Could problems undermine confidence in this staple of defined contribution plans?

Whatever you want to call it,

It sure seems like forced-feeding, with private assets poured down investors’ throats.

A delicacy perhaps, but for whom?

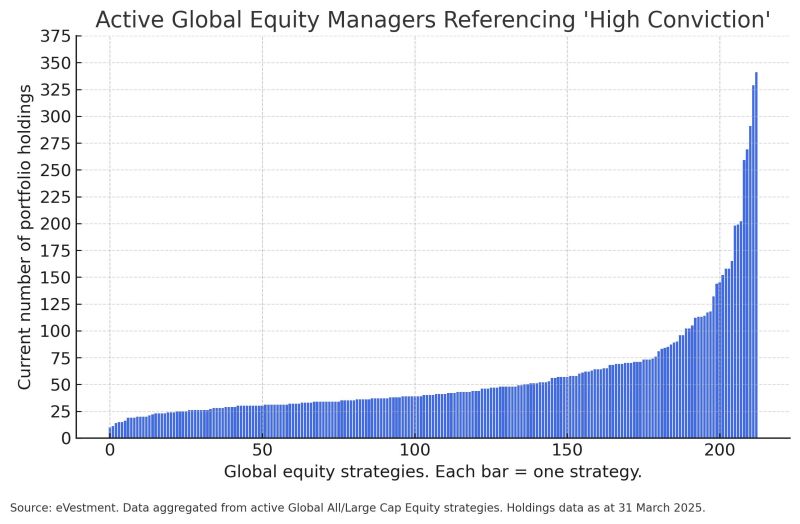

High conviction

Robert Doyle of bfinance posted this graphic on LinkedIn to show how loosely a description can be used, especially one that is meant to indicate confidence. In response, Doyle offers one possible breakdown of company counts across a broad investable universe. What’s your definition of “high conviction”?

Growth and value

Perhaps because the value factor has been on a losing streak for quite a while, the old growth-versus-value debate seems to have petered out. But those categories continue to drive most equity portfolio construction and evaluation — and indexes based upon them still hold sway.

Research Affiliates has released an article, “False Choices, Real Costs: Structural Flaws in the Growth–Value Duality,” which was based upon its more in-depth paper, “Fundamental Growth.” Each provides history on how growth and value indexes have been created — and what the firm sees as the shortcomings of the current state.

Included is a visual which shows the iterations over time (using the same underlying scatterplot of stocks). The last example shown is the one Research Affiliates proposes as the new way of conceptualizing value and growth stocks. It abandons the completeness property, excluding those stocks that are expensive and slow-growing (which generally underperform) from either category.

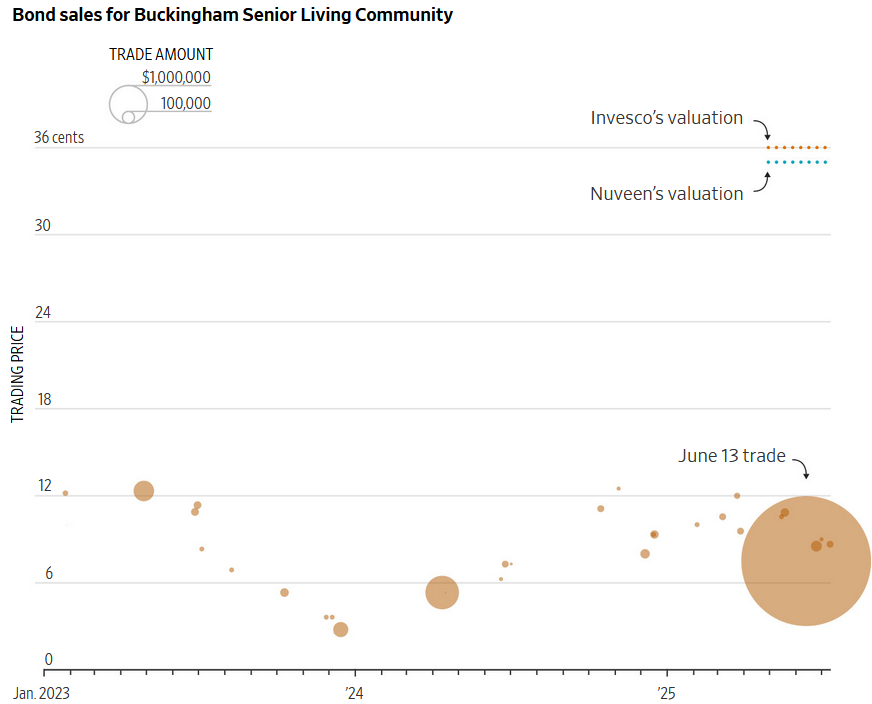

True price

A Wall Street Journal article looked at high-yield municipal bond funds, the ownership of which is “at near-record levels.” Coming off a period when managers funded “all manner of projects,” there are no doubt some stinkers in portfolios, but “true price discovery is only possible when bonds trade in the market.” At least that’s according to a spokesperson for a fund that declined by more than half its previous value when it had to make some sales. And note where a couple of large firms have been marking the position shown above.

A Wall Street Journal article looked at high-yield municipal bond funds, the ownership of which is “at near-record levels.” Coming off a period when managers funded “all manner of projects,” there are no doubt some stinkers in portfolios, but “true price discovery is only possible when bonds trade in the market.” At least that’s according to a spokesperson for a fund that declined by more than half its previous value when it had to make some sales. And note where a couple of large firms have been marking the position shown above.

There are more and more kinds of investments that rely on managers’ marks. Sometimes they’re too high.

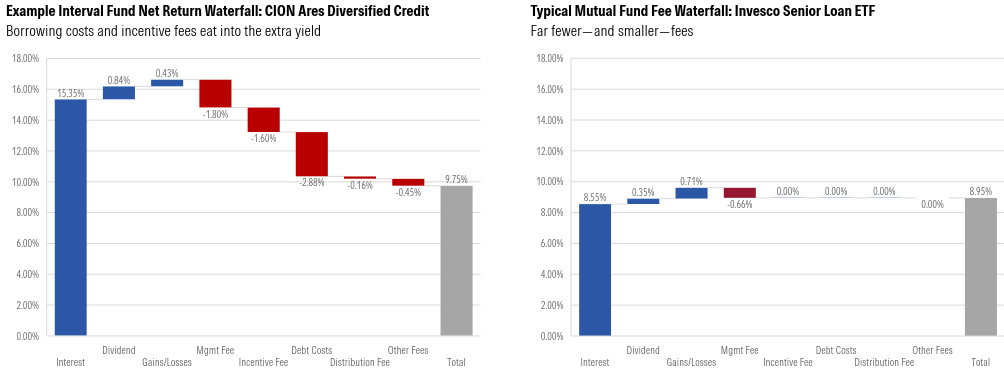

Waterfalls (steep and shallow)

Morningstar’s report, “The State of Semiliquid Funds,” offers a number of charts and tables to illustrate one of the fast-growing areas of the market. This one shows the significant difference in the structure of the return between an interval fund and a standard mutual fund. It’s often said that the only thing that matters is the net return, but the components of it can tell stories.

Other reads

“Venture Capital’s Dissonance Phase: An Opportunity to Rethink & Rewrite the Next Chapter,” Rohit Yadav, CAIA Association.

If the capital input structural layer is sticky and the technology layer is on steroids, the capital outflow layer is under siege.

“The Coin That Landed Sideways,” James Vermillion, The OSVerse. A dialog about expectations, outcomes, and models. (“Soon, you’ll need a model to model your model.”)

“Honey, AI Capex is Eating the Economy,” Paul Kedrosky.

We are in a historically anomalous moment. Regardless of what one thinks about the merits of AI or explosive datacenter expansion, the scale and pace of capital deployment into a rapidly depreciating technology is remarkable.

“Growth Equity: Private Capital’s Overlooked Sweet Spot,” Phil Huber, Cliffwater.

These businesses tend to have cleaner capitalization tables, stronger unit economics, and capital efficiency born out of necessity.

“Zero-sum Thinking and the Labor Market,” Kyla Scanlon, Kyla’s Newsletter. A look at fundamental changes affecting economics, politics, and culture.

“How AI Slop Compromises Investment Decision Making,” Angelo Calvello, Institutional Investor.

The failure of current detection methods to reliably identify AI slop introduces systemic risk into any strategy relying on web-scraped data.

“To Bitcoin or not to Bitcoin: The Corporate Cash Question,” Aswath Damodaran, Musings on Markets.

I believe that it is a terrible idea for most companies, and before Bitcoin believers get riled up, my reasoning has absolutely nothing to do with what I think of bitcoin as an investment and more to do with how little I trust corporate managers to time trades right.

“Key Takeaways from the London ODD Roundtable 2025,” DiligenceVault. An update on current issues in operational due diligence.

“Court in Natixis litigation provides a practical discussion of what constitutes a prudent fiduciary committee process,” October Three.

This case usefully illustrates the axiom that a fiduciary’s ultimate defense against a challenge to its prudence is a prudent and well-documented process.

Eternal truth

“That men do not learn very much from the lessons of history is the most important of all the lessons of history.” — Aldous Huxley.

Flashback: Earnings management

In September 1998 Arthur Levitt, chairman of the SEC, gave a speech about earnings management. It included this:

Increasingly, I have become concerned that the motivation to meet Wall Street earnings expectations may be overriding common sense business practices. Too many corporate managers, auditors, and analysts are participants in a game of nods and winks. In the zeal to satisfy consensus earnings estimates and project a smooth earnings path, wishful thinking may be winning the day over faithful representation.

As a result, I fear that we are witnessing an erosion in the quality of earnings, and therefore, the quality of financial reporting. Managing may be giving way to manipulation; Integrity may be losing out to illusion.

The following few years included some high-profile accounting fiascos, the adoption of Regulation Fair Disclosure, the Global Research Analyst Settlement, and a lot of busted stocks (many busted for good).

More than a quarter century later, with the virtual takeover of “adjusted” earnings in the analytical discourse, where are we on this front?

Mutual fund boards

An early feature of this site was called “Four for Friday,” offering four shorter items linked together by a topic. This one from 2022 includes a quote from an earlier posting that “to be truly effective, a fund board must be an independent force in fund affairs rather than a passive affiliate of management.” In practice, the relationships are pretty cozy, with little effort to evaluate the manager’s organization in ways that might give an indication of the future prospects for the shareholders it represents.

Thanks for reading. Many happy total returns.

Published: July 28, 2025

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.