The most recent essay on this site is “The Research Behavior of Professional Investors.” It considers the need to assess the current state of investment processes in detail, especially given possible adaptations using AI:

That imitation — the swapping of human for machine — is a limited form of improvement, although it may be a realistic first move. The greater mission is coming up with new ways of working that exceed the old, whether they include an extensive use of artificial intelligence or not.

If you aren’t signed up to receive emails when postings are published, you can do so here.

Total portfolio approach

The Total Portfolio Approach (TPA) has been around for a while, but it has had a hard time dislodging strategic asset allocation (SAA), the entrenched model used by most asset owners. In their paper “What is Total Portfolio Approach? A Practitioner Summary,” Redouane Elkamhi and Jacky Lee summarize SAA’s dominance:

SAA’s appeal was not just in its quantitative rigor, but in its institutional utility. It offered clarity to boards, and accountability for performance evaluation. In many ways, SAA provided the architecture around which governance models, organizational structures, and consultant relationships were built.

But that approach involves a series of assumptions “that are becoming harder to sustain in the current investment environment.” The authors stress that a shift to TPA requires a different mindset, concluding that:

Ultimately, TPA is less about perfect planning and more about purposeful readiness — the ability to adapt with clarity, discipline, and intent when the world doesn’t follow the script.

Elsewhere, Roger Urwin writes about the slow development of TPA:

Fast forward 20 years — where are we? The change has been small-scale. TPA is still in a minority position largely because it can only be implemented with a type of stretchy governance that is both very capable and nimble to make a good job of the transition an ongoing challenge. And that type of governance is in very small supply.

And, an article that focuses on the experiences of Sue Brake and Stephen Gilmore, who have been involved in TPA transitions, notes one big stumbling block:

Implementing TPA is hard because it requires an organisation to change its culture by forcing a high degree of collaboration upon investment specialists.

Not all investment specialists react well to such changes as they often have developed their own language and processes to assess new investments during their careers.

The SAA/TPA debate — and the need to create more adaptable organizations — are not going away. Asset owners should be exploring the possibilities. Among the other good references are the TPA hub of the Thinking Ahead Institute and a recent report, “Rethinking Diversification: Learnings from a Total Portfolio Approach,” by Stuart Jarvis of PGIM.

X games

There have been a surfeit of stories in major publications about how individuals have become conditioned to buy the dips in risk markets — and how well it worked in response to the swoon earlier this year. And the most extreme strategies are the hottest.

Bitcoin is setting new highs. The volume of zero-day options is exploding. Small, unprofitable companies are outpacing established ones. As Jason Zweig writes, ETFs are getting narrower and narrower — and more and more leveraged. A Bloomberg article profiled two of the purveyors of those vehicles, where “the cash keeps flowing in and the funds keep launching.” Right now, “targeting [the] degen crowd provides a path to success.”

Saddling up

According to Treasury Secretary Scott Bessent, President Trump is “the most economically sophisticated president, certainly for a hundred years, perhaps in history.” Maybe after explaining the calculus of his tariff proposals, the president could assess the economic implications of the three-percent cut in the federal funds rate he thinks is warranted, starting with whether long-term rates would go up or down if that were to occur.

Bessent and others seem to be auditioning for the role of chairman of the Federal Reserve, which is starting to unnerve market participants who are used to the independence of the Fed that was reasserted by Paul Volcker 45 years ago. Loyalty to any president’s whims by the person in that chair would be a disaster.

Expect a posse of bond market vigilantes to show up if the rhetoric turns into reality.

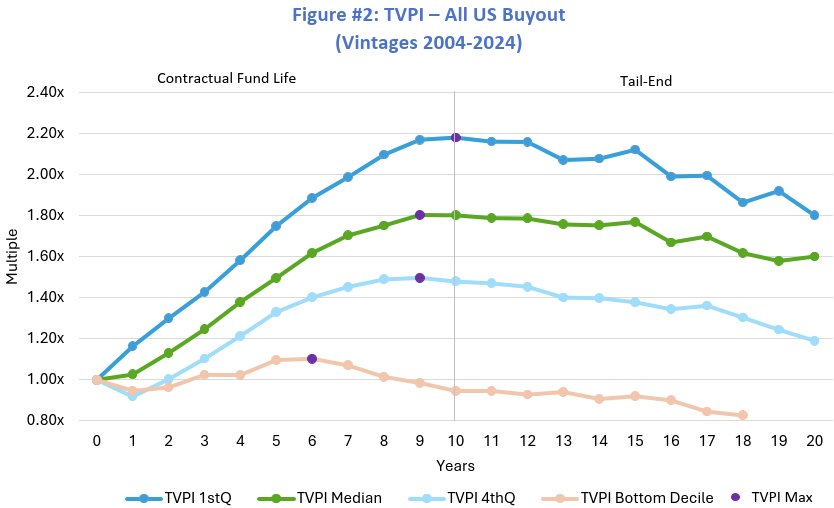

Pulling the trigger

This chart comes from Upwelling Capital Group’s piece “No Country for Old Funds.” It argues that limited partners should be more active in the management of buyout funds, specifically:

LPs should critically evaluate portfolio performance, particularly related to the impact of underperforming or tail-end portfolios.

This chart and others in the report do a good job of providing the case visually. Given the expansion of the secondaries market, Upwelling thinks that new strategies should be employed, including reworking heuristics regarding acceptable discounts to net asset value so that investors can move on to more attractive opportunities when warranted.

The 300

“A group of leading investment professionals” make up The 300 Club. Its reworked website includes a brief summary of the issues it sees in the markets today (including “the consultant-led best practice model” and “the herding of investors into increasingly overpriced assets”). The expressed goal is “Thought leadership for the investment industry;” hopefully this reset is a sign of important contributions to come.

In the haystack

We are on the cusp of a new wave of research tools — within organizations and from existing data platforms and new entrants. Maybe there will even be some created for public use. That’s the case, at least for now, for martini.ai, which bills itself as “Your Corporate Credit Research Assistant.” To test drive it, the CUSIP number of an obscure CCC-rated bond was entered without any other information; the “fast research” and “deep research” summaries produced were quick, useful, and appeared to be accurate. (This is not an endorsement — just another sign of an evolving ecosystem.)

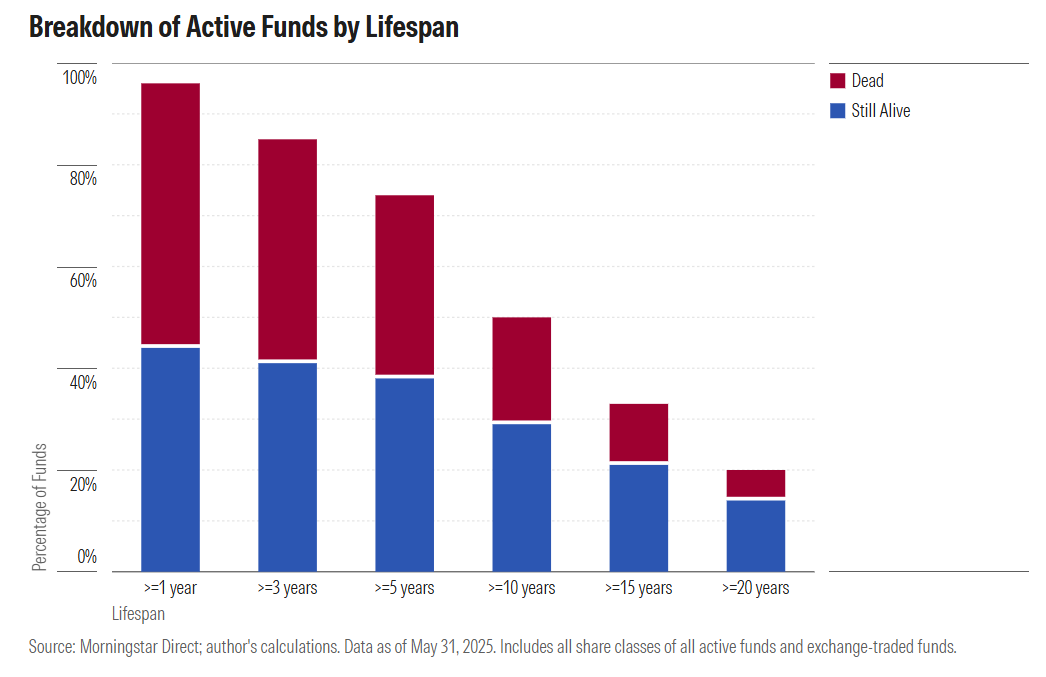

A bad bet

A posting by Jeffrey Ptak of Morningstar, “Bad Bet: Picking Active Mutual Funds,” points out the challenges of investing in those vehicles. First, because of the mean reversion that leads to a small performance dispersion across funds over longer periods (with investors invariably buying during the peaks in relative performance and redeeming in response to slumps).

The second reason Ptak cites is fund mortality. Just when the reversion could move back in a positive direction, the fund sponsor might pull the plug. The chart above documents the lifespans of all funds (ever) that have been in existence at least as long as the time periods shown. So, only about half have lasted ten years or more. Of those that made it that far, about a third are no longer with us.

Other reads

“Should You Diversify, Or Should Companies Do It For You?” Byrne Hobart, Capital Gains.

The corporate finance puzzle around diversification is that there are two ways to get it: a company can buy it for its shareholders by paying a 30% premium to buy out some other public company. Or shareholders can pay a few basis points to diversify into that company (if they want, or to hold on to their shares if they don’t).

“SPVs, Credit, and AI Datacenters,” Paul Kedrosky. Subhead: “How a new credit bubble is building in AI data centers.”

“Effective GP Questioning,” Anthony Hagan, Freedomization.

“Great question,” “We have never been asked that before,” and “You ask the best and most thoughtful questions” are just a few compliments investment managers use to sweet-talk prospective LPs and help keep the conversation positively flowing.

“The Oracle of Tampa and the Modern Portfolio Theory,” Markov Processes. An analysis of the returns over the last decade for Bowen, Hanes, an anomaly among pension fund managers.

“Stronger, Longer, Slower: Why Some Markets Just Keep Trending,” Moritz Heiden, Methods to the Madness.

Do slower biological or logistical production cycles shape how long and how strongly markets trend?

“Saylor’s latest strategy for Strategy: selling new shares to pay dividends,” Craig Coben, Financial Times. As the subtitle says, “Isn’t there a word for that?”

“When Headcount Counts: How Investors are Pricing Scale and Story,” Drew Bowers, et al., S&P Global.

This research introduces a new framework for decomposing deal value [of late-stage AI firms] into three components: industry enthusiasm, workforce scale and firm-specific differentiation.

“Volatility is a Reliable and Convenient Proxy for Downside Risk,” Larry Swedroe, Alpha Architect. A summary of a recent report comparing volatility with a range of downside risk measures.

Be not afraid

“Nothing in life is to be feared, it is only to be understood. Now is the time to understand more, so that we may fear less.” — Marie Curie.

Flashback: Lehman risk management

The last Fortnightly included a flashback to the minutes of a 2006 Federal Reserve meeting that included “one of the greatest indicators of all time” — regarding the looming housing debacle that would set off the financial crisis.

Continuing with that theme, a 2007 slide deck entitled “Lehman Brothers Risk Management” offers the house view of one investment bank at the heart of the subprime mortgage machine. The firm collapsed a year later; but for extraordinary measures, many of its competitors would have done so too.

For a short summary, check out the “Key Themes” on page five of the deck, but leafing through the whole thing is worthwhile for the specifics — as well as a vivid reminder of the need to question the narratives that are served up to you.

Also note the pages of “stress scenarios” at the end. Thirteen past events are used in the scenario analysis, a standard if deeply flawed approach that overwhelms more important qualitative, forward-looking assessments. The urge to tie future possibilities to history is evident earlier in the deck, when the revenue impact for Lehman of each of those events is tallied, as if that was a worthwhile guide.

What wasn’t included among the scenarios studied? A nationwide decline in house prices.

Postings

Among the postings in the archives is “Essential Elements in External Networks,” about the complicated web of sources that feeds us as individuals — and our organizations. One snippet:

The standard inference is that if there is good performance then there is a good process behind it — and a good network which feeds it. But conditions change and a network that is optimized for one environment can be totally out of sync with the next, missing the transition from one to another.

Thanks for reading. Many happy total returns.

Published: July 14, 2025

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.