These curated readings, which come out every two weeks, identify important ideas and debates in the investment world. Original pieces, on pause the last two months, will appear again soon.

But that’s not all we do here. The main objective is helping organizations to identify gaps and provide innovative ideas to seize the opportunities ahead. If that is of interest, schedule a call or virtual meeting today. It will be worth your while.

Compared to what?

Richard Ennis has drawn the attention of the investment industry with his challenges to the orthodoxy of the day regarding alternative investments. One of his papers, “The Demise of Alternative Investments,” was covered in a March edition of the Fortnightly.

It was recently mentioned in a piece from Verdad, which closes with this:

Ennis’s core principles are that simplicity scales and costs matter, enormously. If institutional investors can’t justify the cost of complexity with demonstrable alpha, the rational path is clear: in a world where long-term compounding is paramount, minimizing cost drag is not just a preference — it’s a fiduciary imperative.

And Jeffrey Bronchick of Cove Street Capital shared it and offered a famous Upton Sinclair quote as a commentary on the rush by sponsors and consultants to market alternatives to retail investors:

It is difficult to get a man to understand something when his salary depends on his not understanding it.

Which brings us to a new Cliffwater report which argues that “Alternatives made a significant positive contribution to state pension performance during this century” — challenging Ennis’ evaluations of alt performance. His response to Cliffwater points out the reason for the divergent conclusions: different equity benchmarks.

This brings up a critical issue for asset owners — whom to believe. Not just in this case, but in every one of the many situations where these kinds of disputes linger. Interested parties have different motivations for the presentation of performance information (and one of Ennis’ points is that asset owners are potentially conflicted too, since they use custom benchmarks to gauge their own performance). Plus, there’s always a risk of pointing to past periods and using the results to form a thesis that may be completely off base under different conditions.

And then there is the pernicious problem of using internal rate of return numbers as if they were comparable with time-weighted returns. In many industry reports, those numbers are reported together without any caveats being presented. Often you have to dig into the fine print to identify what’s what, if a clarification can be found there at all.

At this advanced — or what we think of as advanced — stage in the investment industry, we still don’t deal very well with some of the basics.

A ratings factory

Across the investment ecosystem there are a number of small but very successful (and very profitable) entities. What does size indicate and when does it matter?

Those questions are prompted by a Bloomberg article about Egan-Jones Ratings, which has twenty analysts and is based in a “quaint four-bedroom colonial.” Last year the firm rated three thousand investments. Is that too many? Apparently some eyebrows are raised:

Egan-Jones bills itself as the biggest ratings company in private credit, one of the hottest businesses in finance today. Time and again, people familiar with the firm say, it has declared private credit investments to be relatively sound — maybe not gilt-edged AAA, but good-enough BBB.

Is this an echo of the years before the financial crisis, when rating agencies completely misjudged the risks involved in the mortgage market that was then attracting dollars like private credit is today, or is it something else entirely? Inquiring minds should want to know.

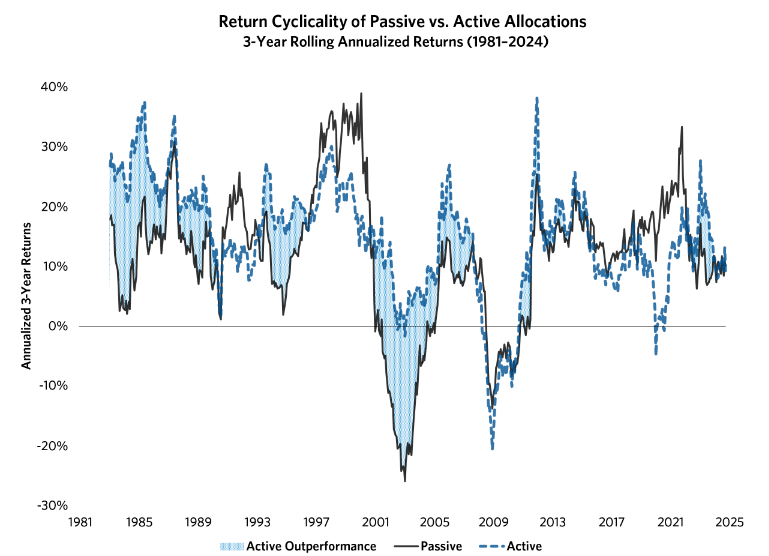

Passive aggressive

Research Affiliates released a paper, “Passive Aggressive: The Increasing Risks of Passive Dominance,” a topic that won’t go away any time soon. (A version with more detailed academic references is available on SSRN.)

You’ve heard the setup before:

Passive products are indifferent to fundamental information, including sales growth, expected earnings, innovation activities, or competitive position within an industry. They allocate based solely upon market price and recent momentum. We explore the growing risks behind the passive boom — and what investors can do about them.

There are several charts of interest, including the one above, which shows that periods when active management outperforms cap-weighted strategies on a three-year basis have essentially disappeared, causing tsunamic flows into passive investing. As you might expect, Research Affiliates argues for rebalancing to strategies using fundamental weighting in response (the approach for which it is best known).

But the existential question is unanswerable:

These market dynamics raise important questions about market efficiency. While we might not be at the tipping point today, the market is flying blind. How much passive ownership will tip the balance: 60%, 70%, more? We simply won’t know until we get there.

What’s in a name?

Fisher Investments, best known for its saturation marketing, has rolled out the website fiduciary.com. Quoted in an RIABiz article, Knut Rostad of the Institute for the Fiduciary Standard says the site amounts to “naked lead-generation,” an example of fiduciary-washing. A spokesperson for Fisher calls it an educational platform.

The article notes that there are 27 references to Fisher Investments on the site and that, as one example of potential conflicts, the firm offers some index tracking funds with fees more than ten times those of identical products from Vanguard.

The word “fiduciary” gets bandied about a lot by providers across the industry, often in questionable ways. Which side of the line do you judge the Fisher site to be on?

Mysteries

A recent Buttonwood column in the Economist was titled “Why investors lack a theory of everything.” (In print it was “Mysteries of the financial universe.”) It concludes:

The complexity of markets is dizzying, and in complex situations even the iron laws of physics can produce surprising, unstable results (think of aeroplane turbulence). More important still, finance is ultimately driven by people, not particles, and they do not always respond to similar stimuli in similar ways. They look at what happened last time, try to do better, anticipate what other traders will do and seek to outfox them. The absence of fundamental laws in markets is frustrating, disorienting — and what makes them so interesting.

Other reads

“What Would Prove You Wrong? The Most Important Question In Investing,” Polymath Investor.

In investing, as in science, how you test your ideas can make all the difference. Treating each investment like a scientific experiment (yes, the whole thing with falsifiable hypotheses and clear criteria for failure), can improve decision-making and protect us from our own biases.

“Death is a Drag,” Jeffrey Ptak, Basis Pointing. A follow-up to the Mauboussin/Callahan paper on drawdowns, this looks at the short-circuiting of the recovery process for mutual funds because of “life-or-death agency risk.”

“Think We’ve Seen the Last +1,000-BPS High Yield Spread? Think Again,” Martin Fridson, Enterprising Investor.

There are valid rationales for a strategic allocation to high yield bonds, including their high current yield and low correlation with both investment grade bonds and equities. . . . High yield asset gatherers consequently have no need to promote the asset class based on assertions that may not stand up to scrutiny, such as, “We will never again see a +1,000-bp spread.”

“The investment industry is a placebo,” Kris Abdelmessih, Moontower. How long do you have to wait to know that a factor is no longer significant?

“Flyover Country, Operating Partners, and The Deal-by-Deal Play,” Shahrukh Khan, Cash and Carried.

What character does capital take on when it’s structured primarily for permanence, without considerations of social prestige?

“Created Value Attribution Whitepaper,” PJ Viscio and George Pushner, Kroll. Subtitle: “Whither Deleveraging? Implications of Higher Interest Rates for Private Equity Value Creation.”

“Moats, Money, and Management’s Mettle,” Todd Wenning, Flyover Stocks.

Make no mistake: culture and character evaluation is hard. Relevant and reliable information can be hard to come by. This type of analysis is qualitative and subjective, which can lead to biases clouding your judgement.

“Quant Firm’s $1 Billion Code Is Focus of Rare Criminal Case,” Chris Dolmetsch, Bloomberg. Is the value of trading code “ephemeral”? (Is every investment process?)

“After 6 weeks of intensive due diligence . . .,” Itamar Novick, LinkedIn.

This is the intellectual property theft horror story that VCs systematically use.

Keep at it

“It is better to fail in originality, than to succeed in imitation. He who has never failed somewhere, that man can not be great. Failure is the true test of greatness.” — Herman Melville.

Flashback: Hedge funds

Normally in this space there are flashbacks to specific articles. This time, we bring you the 25th anniversary edition of Hedge Fund Alert, which is a compilation of excerpts from throughout the publication’s history.

You’ll see the early moves of boldfaced names, get a sense of the ups and downs of the business over a quarter century, and be reminded of strategies that went down in flames (mutual fund timing, subprime, Madoff, Allianz, etc.).

Postings

All of the previous postings are in the archives.

From 2022, “Looking in the Rearview Mirror” leverages the liability-driven investing (LDI) spasm to examine industry risk management practices. Among them:

“Stress tests” are popular, but they often represent five or ten landmark events — what would happen if we relived a past spasm. What’s missing? A qualitative dreaming of what might go bad in a big way because of the particular excesses in valuation, vehicle structuring, or economic (or geopolitical) events of the moment. And not much attention is given to the extremes of the projected distribution, even though markets are creatures with fat tails.

Thanks for reading. Many happy total returns.

Published: June 16, 2025

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.