In his most recent book, Aswath Damodaran used the corporate life cycle to map out critical issues in corporate finance, value and price, investment philosophy, and managing a firm. It’s the topic of the latest Investment Ecosystem essay, “A Panoramic Look at the Corporate Life Cycle.”

Also new is a compilation of the concepts for analyzing investment organizations that have been referenced individually in previous issues of the Fortnightly. Plus, a 2012 posting on “assumption hunters” published on the precursor to this site was incorporated into a new article by Grant McCracken.

Expected value

Michael Mauboussin and Dan Callahan have produced a wide-ranging report on expected value, “Probabilities and Payoffs.” It addresses a host of issues of importance to investment professionals. Fundamentally,

Feedback in investing and business is impeded by noise and lag time between forecast and outcome. The way to deal with noise is to keep score using probabilities instead of words. The way to deal with the lag time is to break down a thesis into subcomponents that are relevant over shorter time horizons.

A variant perception, or investment thesis, can almost always be distilled into outcomes that are objective, within a specific time horizon, and occur with an estimated probability.

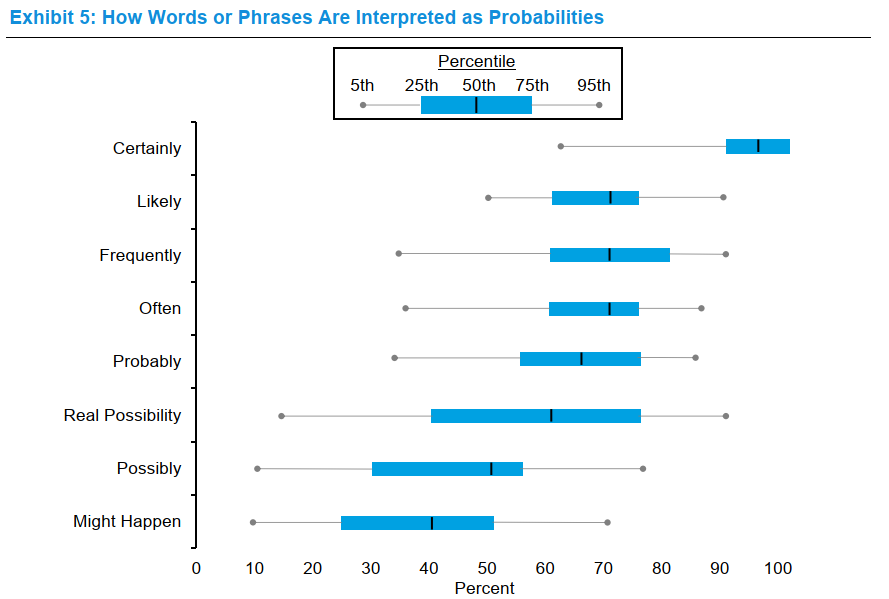

Regarding “using probabilities instead of words” (which, remarkably, is very rare in the investment industry), if you haven’t done the exercise at probabilitysurvey.com, you should. Here are the ranges of probabilities that others have assigned to a few of the many phrases on the survey:

The words that mean something to you mean different things to other people. Use numbers.

That’s only one of the many insights in the report, which can serve as a framework to evaluate investment philosophy and process. It deals with the essential “why” and “how” questions that should underlie those broader concepts — and those questions don’t get asked nearly enough.

Fessing up

Warren Buffett’s annual letter to the shareholders of Berkshire Hathaway demonstrates how he is different from other company managers. There are examples of that fact throughout, but the very first topic — about giving shareholders the good and the bad in a straightforward fashion — shows it in spades.

That is very much not the way of the world, which Buffet has seen for himself:

I have also been a director of large public companies at which “mistake” or “wrong” were forbidden words at board meetings or analyst calls. That taboo, implying managerial perfection, always made me nervous.

Managerial perfection is not to be found anywhere and, as we say around here, all organizations are messy. Assuming otherwise is foolhardy.

Highly engineered profits

Also Buffett:

EBITDA, a flawed favorite of Wall Street, is not for us.

As if on cue, a Bloomberg article recounted the “disastrous buyout” of Schur Flexibles, which imploded not long after it was sold by the private equity firm Lindsay Goldberg. At issue: the statements of “highly engineered profits” (read EBITDA) at the center of the deal.

It’s important to understand “who’s doing the math” and what adjustments find their way into EBITDA. That it also underscored in a posting from Stephen Clapham of Behind the Balance Sheet, “The Great EBITDA Illusion.”

He shows a steady increase over time in adjustments to EBITDA and cites a report from S&P’s Leverage Finance Group:

Our six-year study on EBITDA addbacks appears to shows a positive correlation between the magnitude of addbacks at deal inception and the severity of management projection misses.

Commenting on the Bloomberg article, Byrne Hobart said:

Sometimes, there are expenses that don’t tell you much about the state of the business, and should be removed from calculations of the company’s long-term earning power. But if management has broad discretion about what those are, and goes looking for a counterparty that will avoid asking too many difficult questions about where the numbers come from, it can lead to a disastrous deal.

In the end, it comes down to due diligence — and don’t expect auditors and investment bankers to do that for you.

The natural language of finance

Up until the introduction of ChatGPT, natural language processing (NLP) was the most prominent artificial intelligence application in investment analysis. While now overshadowed, it continues to be of interest.

A new paper, “The Natural Language of Finance,” by Gerard Hoberg and Asaf Manela, covers the strengths and limitations of NLP. While it is written for academicians, it is of value to investors, especially the section on asset pricing.

Much of the work on NLP has been used to measure signals in corporate communications, including conference calls, annual reports, etc. As mentioned in previous postings here, that has led to a cat-and-mouse game between managements and investors. Another paper, from Jonathan Berkovitch, et al., argues that “firms strategically embed sentiment within corporate disclosures, and investors incorporate this sentiment into stock prices and trading activity.”

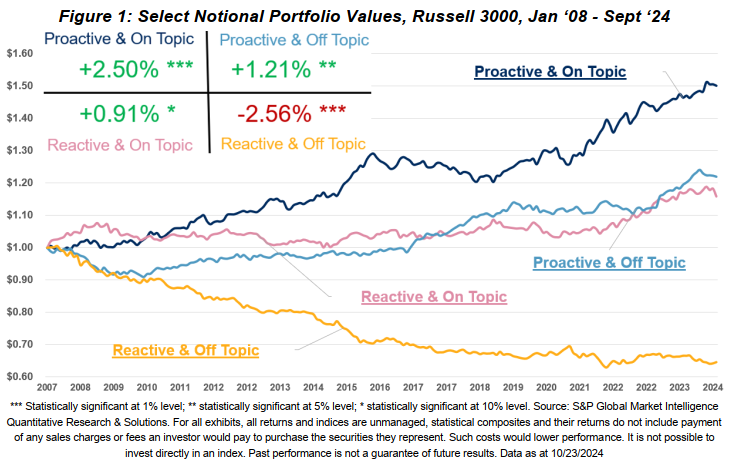

A report from S&P used NLP to look at questions from analysts about topics not addressed in the prepared remarks for an earnings call. The analysis produced the calculations and chart below that shows responsiveness to the questions (proactive or reactive) and whether the executives stayed on topic when answering. Striking.

Convergence concerns

Convergence between public and private investments is all the rage and product purveyors are more than willing to feed the ducks when they are quacking.

Three articles on ETFs worth reading:

~ Jeffrey Ptak of Morningstar wrote about ERShares Private-Public Crossover ETF and its SpaceX investment, which conveniently was marked up 37% a week after being added to the fund. But the devil is in the details.

~ Eric Platt and Will Schmitt of the Financial Times covered the odd goings-on last week, when the SPDR SSGA Apollo IG Public & Private Credit ETF started trading, only to have the SEC raise questions about the fund after the fact. Brooke Southall’s look at the issues for RIABiz provides more information — and more concern — about the “back channel” method for the fund filing and serious potential issues for those involved.

A new CAPE

According to a report from Research Affiliates, the cyclically adjusted price-to-earnings ratio (CAPE) has “performed the service of returning to the tried-and-true principle that the best predictor of future returns is starting-point valuation.” But the firm thinks that there’s something even better: the “current constituents CAPE.” The revised measure uses the earnings history of the current members of the S&P 500, not the historical earnings of that index, in an attempt to mitigate the distortion from the S&P committee’s inclination to “buy high and sell low” when making changes to the index.

Other reads

“On Loopholes & Fiduciary Duty,” Steve Novakovic, CAIA Association.

I think it would be great to close the carried interest loophole, not because I wish GPs made less after-tax earnings, but because I’d like to see which GPs decide that their after-tax earnings are the most important factor in the investment process. Then LPs can really see which GPs have a client-first mindset and which GPs are in it exclusively for their own benefit. Maybe the trade associations were onto something. Closing the carried interest loophole would stifle investment, just not in the way that they portray it. It would stifle investment to GPs who are selfish actors.

“PIK and Choose,” Phil Huber, Cliffwater (via LinkedIn). On the “lightening rod of debate” in direct lending.

“Time to come out of the turnover closet,” Simon Evan-Cook, Citywire New Model Adviser.

So, here’s the challenge to us fund buyers: Is the ‘high turnover bad/low turnover good’ belief just a lazy assumption?

“Shoe Leather Alpha,” Christopher Schelling, LinkedIn. Looking for winners? You need to be willing to do the hard work of finding the undiscovered (and often “unproven”) gems rather than following the crowd.

“CalPERS board ponders the risks of TPA,” Sarah Rundell, Top1000Funds.

Under its current SAA, CalPERS currently has 11 different benchmarks. Gilmore reflected that it is sometimes hard to see if the team has done a good job with so many benchmarks because they create different nuances. “With a reference portfolio it is much simpler; the question is: ‘Has management done better than a simple liquid portfolio,’ ” he said.

“The looming advisor shortage in US wealth management,” Jill Zucker, et al., McKinsey. Advisory firms have been been on a roll for the last couple of decades, but there are “clouds on the horizon.”

“Women (and men) in finance are not typical,” Renee Adams, SSRN.

If financial firms generally do not hire women, perhaps out of concern that women will not take enough risk, then the women who end up being chosen for a position in finance may not be as risk averse as other women.

“America’s Most Famous Stock-Market Measure Is More Broken Than Usual,” James Mackintosh, Wall Street Journal. In which a reporter for the flagship paper of Dow Jones calls out the index that carries its name.

Keep moving up the curve

“The beautiful thing about learning is that nobody can take it away from you.” — B.B. King.

Flashback: GFC

A pair of articles published late last week raised the specter of the financial crisis. “Money Managers Return to a Levered Trade That Went Bust in 2008,” by Lu Wang and Yiqin Shen in Bloomberg highlighted the increasing popularity of portable alpha strategies:

A diversified investment strategy that seeks to juice returns through leverage is finding new love among big money managers — more than a decade after it blew up during the 2008 financial crisis.

According to the article, “advocates say they can make it work this time by improving transparency and liquidity.” The piece ends with a quote from one such advocate of portable alpha:

It allows precise, systematic exposure management and the flexibility to integrate various strategies to meet a desired risk-return profile.

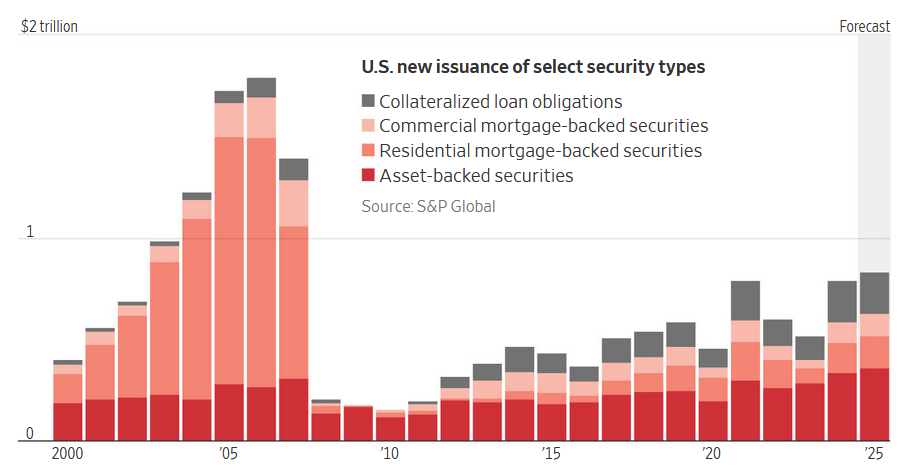

The headline of the other article, by Matt Wirz and Justin Baer for the Wall Street Journal: “They Crashed the Economy in 2008. Now They’re Back and Bigger Than Ever.”

“They” being asset-backed securities, which have already eclipsed last year’s issuance. And “they” being the hoards of people who set the attendance record last week at the structured finance conference made famous in The Big Short.

Harkening back to 2008 is easy pickings for the media, but echoes of increased leverage and sliced-and-diced credit exposures do make one wonder whether people are dancing to the same old music even though it has a new beat. Time will tell.

Postings

All of the postings are in the archives, including one called “In the Belly of the Beast,” which summarizes two accounts from people on the front-lines during the late 1990s, one of whom came in “as an idealist and left a cynic”:

I was burnt-out, exhausted, and depressed about the current state of affairs. I’d been both very right and very wrong in my career, but my industry was in a shambles, thanks to a potent mix of overcapacity, underwhelming demand, and good old-fashioned fraud.

Thank you for reading. Many happy total returns.

Published: March 3, 2025

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.