Happy New Year.

A few things you may have missed during the holiday quiet period:

The last Fortnightly featured some of the most popular postings from 2024.

Our most recent essay referenced some examples of academic research and posed questions for practitioners.

A LinkedIn article discussed using “a show of hands” in presentations and meetings to gauge audience beliefs — and gave some examples of simple yet powerful questions. (Quick, are interest rates high or low?)

The Investment Ecosystem is now on Bluesky, posting interesting links and visuals.

On to the readings.

Around the clock

In his newsletter False Positive, Miles Kellerman explains how “measurements of time are essential to today’s capital markets,” and that “now markets are experiencing another change to their space-time continuum: the advent of 24/7 trading.” And “24/7 trading changes everything.”

Not only will there be regulatory issues, Kellerman writes, but political ones. Imagine how the financial crisis (or other market spasms) would have played out if there hadn’t been the natural breaks offered by closing the markets for most of each day — and all weekend.

There are also technical concerns about how clearing and settlements processes might be affected under a different set of rules. And, critically, disrupting the existing system could have unpredictable implications for the behavior of different kinds of investors and for the evolution of the investment ecosystem.

Kellerman’s conclusion:

For hundreds of years, we’ve decided those hours should be strictly limited. And now those limitations are being withdrawn. The implications, both for our markets and our politics, will be seismic. Because the best strategy for a game is very different when it has no end.

AI and investment decision making

Angelo Calvello wrote an opinion piece for Institutional Investor called “Investment Management in a Box.” In it he states, “Today it’s possible to use artificial intelligence to create the full range of mission-critical organizational functions necessary to run an asset allocator, asset manager, or investment consultant.”

The idea goes beyond using a single large language model to creating a multiagent system (MAS) that replicates the capabilities necessary to operate an investment function. For those contemplating how organizations will be designed in the future (a central concern here at the Investment Ecosystem), the ideas are worth examining in depth.

To take advantage of the opportunities presented, Calvello sees the need to overcome our “algorithm aversion”:

The primary obstacle to adopting MAS and advanced AI is not technical or operational but rather the behavioral bias that says investing is inherently a human activity.

It would seem that trust in AI-dependent systems will come in fits and starts (with any significant failures or enforcement actions having the potential to disrupt adoption trends). Recent research from Francesco Stradi and Gertjan Verdickt shows that “although investors update their return beliefs in response to [forecasts], they are less responsive when an analyst incorporates AI.” Danielle Labotka of Morningstar cites other evidence about the “disclosure effect” that causes a lowering of trust, but she recommends that investment advisors be transparent with their clients about the use of — and the benefits from the use of — AI.

Alts for the masses

The headline for a recent Jason Zweig column in the Wall Street Journal: “You’re Invited to Wall Street’s Private Party. Say You’re Busy.” It begins:

Hold on to your wallet. Wall Street is gearing up for a sales push that could enrich the middlemen and impoverish you.

Zweig argues that when it comes to alternative investments, the “potential virtues come at the cost of higher fees, greater risk, more conflicts of interest and less disclosure.” And illiquidity. But circumstances have made the retail market particularly attractive now for the purveyors of such products:

As the managers of alternative funds have struggled to resell a glut of overpriced assets, they’ve also been stymied trying to convince big clients to add more money.

No wonder there’s an intensifying push to strip away the traditional protections for smaller investors.

While Zweig urges individuals to proceed with caution when considering private investments, in a presentation to “an SEC advisory committee on the mainstreaming of private assets for retail investors,” Phil Bak champions more radical improvements to the existing system. He thinks that regulations need to change — and technology and transparency need to improve — so that private assets can “benefit from the same opportunity for price discovery and liquidity” as is available in the public markets.

The industry battle to get private investments to individuals is being waged on two fronts: advisory firms and defined contribution plans. Regarding those plans, the Defined Contribution Alternatives Association released a paper, “Modernizing Retirement Savings.” As could be expected from an advocacy organization, it reports that “it is widely agreed that the inclusion of alts in DC retirement savings plans can strengthen the retirement outcomes of participants.” A more balanced view comes from Aaron Filbeck, writing in the Investments & Wealth Monitor about “The Complex Case of Integrating Private Markets in Retirement Plans.”

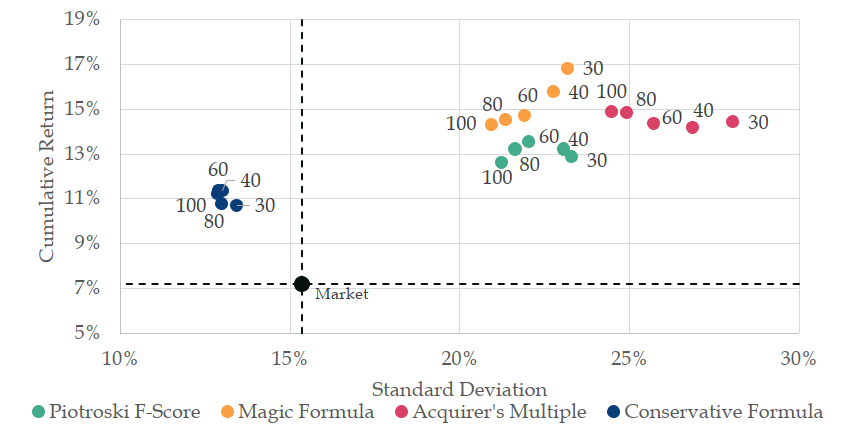

Formula investing

In “Formula Investing,” Marcel Schwartz and Matthias Hanauer evaluate four popular investing approaches. The results for the period 1963 to 2022 are shown above (the multiple dots indicate the different number of stocks included in the long-only portfolios that were created).

While “all formulas exhibit predictive power . . . no single formula consistently dominates across performance metrics.” And there are periods when all of them trail the market. Plus, the results have not been as strong this century as they were before:

While all formulas remain successful for concentrated long-only portfolios in the post-2000 period, we observe some performance decay relative to earlier periods, underscoring the need for continuous innovation in investing strategies.

Revaluation alpha

Rob Arnott of Research Affiliates writes that while we are told that past performance is not predictive, “we are relentlessly tempted to believe otherwise.” The critical question is:

What aspects of past returns are (at least modestly) predictive of future returns, what aspects are perverse predictors, and what aspects are pure noise?

Arnott distinguishes between structural alpha, revaluation alpha, and noise, asserting that revaluation alpha (which he terms “pernicious”) causes investors to misjudge probable future outcomes. Unfortunately, there are incentives for academics and investment organizations to promote their good results without noting the potential reversals in valuation ahead.

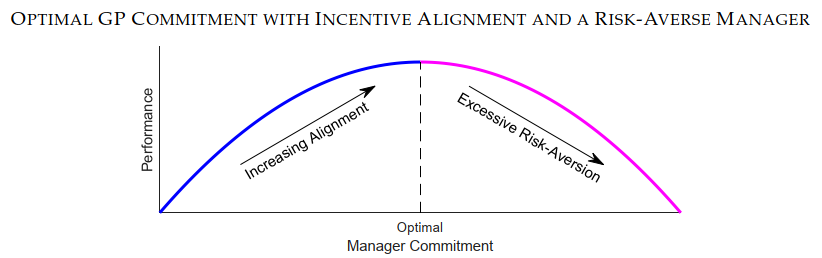

Skin in the game

This stylized image comes from “Do GP Commitments Matter?” a paper by Gregory Brown and William Volckmann for the Institute for Private Capital. It seeks to “fill the gap in research” regarding the size of commitments and fund performance:

Despite the ubiquity of the practice, and the belief that it aligns GP-LP incentives, there is almost no large-sample empirical analysis of GP commitments.

The study pegs the optimal commitment in the 10-13% range, “which is substantially higher than the average commitment rate of 3.5%.”

Other reads

“Optimus Prime Brokerage,” Daniel Davies, Financial Times.

If this consultation exercise ends up with a requirement for big funds to show their cards to their prime brokerages, then that will not only make a big prime brokerage operation an incredible competitive advantage, it will also hugely tilt the playing field in the favour of the sellside versus the buyside.

“2035: An Allocator Looks Back Over the Last 10 Years,” Cliff Asness, AQR. A clever look at expected returns for the next decade (and how existing norms may be brought into question).

“FY24: Princeton & Yale Returns Dragged by VC & Lack of Stock Exposure, Harvard boosted by Tech & Hedge Funds,” Markov Processes.

By our count, it was the first time that the average school (and the simple 70/30) has beat the Ivies two years running since fiscal 2003 — when our records for all Ivies begin.

“The CEO Scorecard: How Directors Select a CEO When They Have Real Skin in the Game,” A.J. Galainena, et al., Stanford Business. The ways in which ValueAct tries to improve succession processes so that they don’t “devolve into a series of subjective arguments.”

“What LPs Really Like About Their Favorite GPs,” Anthony Hagan, Freedomization.

An allocator is usually only ready to be overly bold about a manager after enduring (from other GPs) a lot of hurt, a lot of betrayed trust, a lot of soul searching, and has spent many years painfully shedding the scales of naivete.

“Doing deals or constructing portfolios,” Christopher Schelling, LinkedIn.

Planning doesn’t always seem as sexy as doing deals, but boring is what works.

“What company’s past reveals the future of OpenAI?” Walt Hickey, Sherwood. Investors like to look for analogues — here are thirteen ideas of company stories that OpenAI’s could end up resembling, from Adobe and Visa to Taco Bell and Lehman Brothers.

“Persistent Alpha: Lessons from the Pod Shops,” Daniel Rasmussen, et al., Verdad.

We think it’s possible that the pod shops are succeeding not just because they have access to exceptional talent but because of their disciplined execution. It’s possible that their edge lies in dynamic capital allocation to short-term alpha generators, rigorous risk management using advanced risk models, and the strategic use of leverage to amplify returns. If those are indeed the core building blocks in the model, there’s no reason it couldn’t be reengineered using the thousands of public managers plying their trade in liquid funds.

“Our 2024 Hedge Fund Analyst Christmas List,” Edwin Dorsey, The Bear Cave. An annual list of resources for analysts (of all stripes).

Look for the little things

“It’s worth remembering that it is often the small steps, not the giant leaps, that bring about the most lasting change.” — Queen Elizabeth II.

Flashback: Rivers of money

In 2010, Venkatesh Rao wrote a piece, “Ancient Rivers of Money,” on his blog, Ribbonfarm. His river metaphor provides a good visual representation of the changing nature of cash flows in the economy (and the behavior of organizations that rely on them for life):

Some rivers of money are very old and very stable. You can at most fight to displace others from prime positions along the banks. Others are new and unstable and may change course frequently, creating and destroying fortunes through their vagaries.

(A hat tip to Taylor Pearson’s link to Rao’s posting in The Interesting Times and his extension of the ideas.)

While Rao does not reference the investment industry per se, his concept is a useful one in studying it. What rivers are drying up? Where are new brooks being formed that will be mighty some day?

Postings

All of the postings are available in the archives. While they are sorted into categories, most have broad application in the industry and are evergreen.

For example, take a 2021 posting, “Resisting the Force Field of Observed Performance,” which deals with a powerful force in decision making — as long as performance pleases, qualms are ignored:

The reluctance to act while the numbers look good is reinforced by others, including investment committees, advisors, clients, and other interested parties. No one wants to step away from a winner over “concerns.”

Thank you for reading. Many happy total returns.

Published: January 6, 2025

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.