The most recent posting on the site deals with a common question these days: whether to have a meeting virtually or in person. The question applies across investment roles, although in this case it addresses the due diligence of asset managers. Regarding onsite visits:

There is a big difference between conducting a visit to confirm what you already believe and being open to new evidence and possibilities. The design of a visit should maximize discovery and push on the boundaries of transparency — not follow a standard playbook.

Where can’t you go? Who can’t you see? What won’t they talk about? Why?

On to the readings.

Institutional imperative (public equity)

A December 6 Wall Street Journal article by James Mackintosh began in this way:

Here are two particularly scary forecasts for investors: Goldman Sachs thinks the S&P 500 will make just 3% a year over the next 10 years, as Big Tech dominance eventually falters. Bank of America expects 0%-1% a year for a decade, a catastrophic investment prospect.

Their conclusion: Buy stocks anyway, because the next year looks great.

Elsewhere, BlackRock’s 2025 outlook opens with an observation: “Historical trends are being permanently broken in real time as mega forces, like the rise of artificial intelligence (AI), transform economies.” It then says that “2024 has reinforced our view that we are not in a business cycle.” (The quotes are from the online version; the PDF is slightly different.) The bottom line: overweight U.S. equities.

On the flip side of the bullishness, the list of classic warning signals (in addition to BlackRock’s revocation of the business cycle) includes a variety of valuation levels approaching or exceeding previous peaks; bearish analysts throwing in the towel; the demand for leveraged exposure to large cap stocks rocketing higher; speculative plays thriving; and the U.S. market “sucking money out of the others.”

For professional investors measured against benchmarks (most all of them), this presents a dilemma. You don’t want to be too late, but you can’t afford to be too early. The institutional imperative plays on.

Institutional imperative (private equity)

You might think that the sloppy times in private equity recently would lead to some increased caution on the part of investors, but a variety of surveys of large asset owners show that more of them are planning to increase their exposure than decrease it.

A recent report from bfinance shows the satisfaction rating regarding private equity falling from 94% in 2022 to 69%, almost identical to the 68% that expect to increase or maintain their exposure to the strategy in the next 18 months. That’s versus 8% that want to reduce it (the remaining quarter of those surveyed don’t invest in private equity).

A Financial Times article cites a survey of public and sovereign wealth funds that showed a slightly higher level of asset owners planning to reduce private equity, but still a very small percentage. Why?

“Public funds are going to continue in aggregate to allocate more to private markets until something bad happens,” said Paul O’Brien, a trustee of the $11.2bn Wyoming Retirement System. “Nothing bad has happened yet.”

As popular strategies do, the “endowment model” has spread far and wide from its roots. Never one to pull his punches, Richard Ennis sees the ongoing love affair with private markets at those pioneering institutions as symptomatic of an Endowment Syndrome, marked by “(1) denial of competitive conditions, (2) willful blindness to cost, and (3) vanity.”

What are the chances that endowments will reverse course and that others will follow once again?

Family offices

Sharon Schneider of Integrated Capital Strategies created a LinkedIn post in which she wrote, “There’s really no such thing as a three-generation Single Family Office.” She outlines the strains that develop because “the structures, legal entities, trustees, advisors and norms of the family office established by their grandparents” don’t fit with the disparate interests of the “cousins” (“they contain multitudes”).

As if in response, Morgan Stanley published a report, “The Future-Ready Family Office.” It provides the firm’s prescription for the sustainability of a family office, with recommendations in four key areas: governance, staffing (including what to outsource and what to keep in house), investing, and education. Regarding Schneider’s concerns:

Often, the purpose of a family office is dictated by the first generation’s or founder’s goals and preferences. But, as the family grows and evolves in subsequent generations, its needs and priorities may change. Unless the family office pivots accordingly, it may become set in its ways, leading to missed opportunities, instability or fracturing among the family — ultimately creating risk for the family office and family.

Also on the family office front (and also on LinkedIn), Craig Dandurand of the Tuckwell Family Office shares a presentation summarizing the differences he found moving from an institutional asset owner to a family office.

Securities lending

Most of the time, securities lending is thought of as a way to add a little extra return on top of a portfolio. State Street, one of the big players in that business, would like you to look at it more broadly. Thus, its report, “The ‘Sharpe’ Point of Securities Lending,” offers information on the returns, standard deviation, skewness, Sharpe ratio, and Sortino ratio of the strategy — in the hopes that you’ll be enticed by the “efficiency frontier expansion” on offer.

(The data used start in 2008. That’s an interesting time to pick, especially since some exhibits begin with January of that year and some with October — and the MSCI ACWI sample, used for comparison, starts in March 2009.)

The value of information

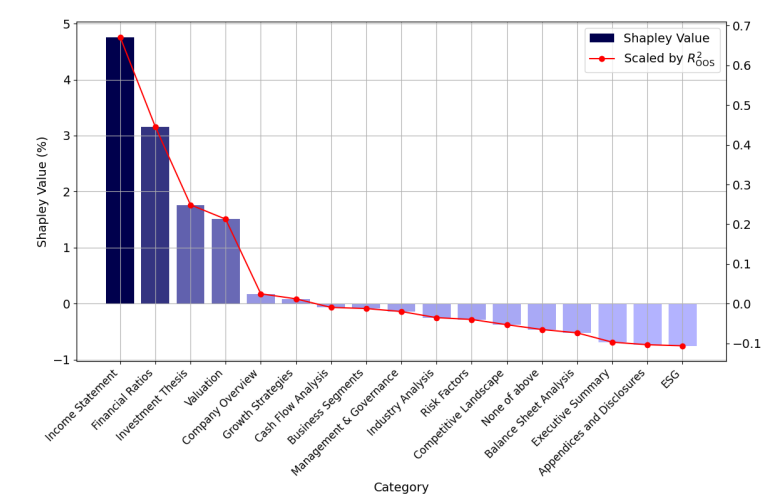

In the study “The Value of Information from Sell-side Analysts,” Linying Lv tries to answer the question, “Do analysts generate value for their clients, or are they merely peddling expensive noise?”

Academics are increasingly using large language models to evaluate written investment reports, which “investors consistently rank . . . as more valuable than earnings forecasts and stock recommendations.” Those latter indicators have anchored the previous assessments of the contributions of analysts.

Using more than a hundred thousand analyst reports, the author tapped the large language model to address a variety of questions, including assessing “how much each topic within the reports contributes to explaining stock returns.” That ranking is pictured in the chart above.

Other reads

“Democratizing Risk,” Roland Meerdter, LinkedIn.

True democratization requires more than access alone; it demands a system that supports stability alongside participation. Fund managers need to carefully balance liquidity with stability through prudent redemption policies, resilient structures, and investor education on the risks of private markets.

“TSMC: Totally Stupid Market Chaos,” Owen Lamont, Acadian. Why is the stock violating the Law of One Price (in a significant way)? What does that say about the market environment?

“Time-varying asset allocation,” Todd Schlanger, et al., Vanguard.

These potential value-added returns are made possible by the fact that returns for stocks, bonds, and their sub-asset classes deviate materially from their long-term averages over the medium term, defined here as the next decade; and that there is a directional relationship between the “fair value” of these asset classes at a given point in time and their future realized returns.

“The Whiz Kid Who Made Billions for Yale Is Rethinking His China Strategy,” Rebecca Feng and Juliet Chun, Wall Street Journal. From the wisdom of saying “I don’t know” to “the gamble that made a career” to changing strategy in response to investors’ concerns about overexposure to China amid political risks.

“The secretive world of McKinsey’s $48 billion hedge fund,” Laith Al-Khalaf, Sunday Times.

McKinsey Investment Office (MIO Partners) started out as a pension plan for the firm’s partners, but has morphed over the decades into an investment juggernaut.

“Mutual Funds & Unicorns,” Jack Shannon, Morningstar. In a piece subtitled “A fruitless marriage,” the firm concludes that “mutual fund managers do not appear to be skilled private-company stock-pickers.”

“The Worst Time To Conduct Due Diligence,” Anthony Hagan, Freedomization.

There is something inherently unnatural about the ready-set-go fundraising protocol most of us have been subliminally trained to accept and follow.

“Market Concentration: How Big a Worry?” Goldman Sachs. Four interviews from different perspectives (and a number of exhibits) regarding one of the hottest market topics.

“AQR’s Cliff Asness Says AI Has Now Taken Over Parts of His Job,” Justina Lee, Bloomberg.

“AI’s coming for me now,” he said. “It turns out it’s annoyingly better than me.”

Know when to hold ’em

“Blessed is the man who, having nothing to say, abstains from giving us wordy evidence of the fact.” — George Eliot.

Flashback: Hedge fund evolution

In 2018, David Finstad wrote a piece for Institutional Investor, “Have Institutional Investors Spoiled the Hedge Fund Party?” It is a good summary of the evolution of the “industry” to that point, as performance “declined precipitously” from its heyday and assets under management “exploded.”

Among the changes Finstad identified:

The makeup of hedge fund investors shifted from return-seeking high-net-worth individuals and family offices to large institutions that had more modest return expectations and were more focused on risk management and diversification benefits.

For investors, the biggest benefit has been a reduction in funds that have blown up or been involved in fraudulent activity. The biggest negative has been degradation in alpha received from their hedge fund investments.

He felt that “institutional investors [were] incentivized to keep their jobs rather than serve their funds’ best long-term interests.” Six years on, not much has changed. The pod shops have come to dominate the landscape; their pass-through expenses from an unbridled “war for talent” mean that “the value proposition of hedge funds is questionable today,” just as it was in Finstad’s telling.

Postings

All of the previous postings can be found in the archives.

One example, “Identifying the Complexity Risks in an Organization,” ends this way:

Under any circumstances, market stress can amplify organizational stress and business model stress. Increased complexity of whatever sort means that periods of pressure can be more unpredictable than they otherwise would be. In all respects it pays to gauge the payoff for complexity and the potential downsides involved, so a multidimensional analysis of it should be part of your strategic planning process.

Thank you for reading. Many happy total returns.

Published: December 9, 2024

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.