Thursday is Thanksgiving Day in the United States, making it a perfect time to thank you for reading and for passing along our material to others. We truly appreciate it.

If you missed it, the latest posting was about “Communicating Across Time.” We all have our tried and true ways of communicating, but they can become out of date, so we “need to consider whether our messages are heard, whether they resonate, and, yes, whether they blend with the zeitgeist.”

On to the readings.

Private fund structures

A posting from Goldman Sachs, “Choose Your Vehicle: A Closer Look at Private Market Fund Structures,” begins:

We do not believe there is a universal best choice between private market fund structures. The decision involves a set of trade-offs along four key dimensions. We believe the assessment should reflect the outcomes of an investment program, rather than a single fund.

The four dimensions are liquidity, complexity, product availability and access, and performance. Goldman considers evergreen funds to have the advantage in the first two categories and drawdown funds to come out on top for the last two. (Regarding performance, a Neuberger Berman piece comes to the opposite conclusion.)

There has been an increased interest in evergreen funds of late, because of the shortcomings in drawdown funds that Goldman identifies; the desire on the part of some investors to have vehicles that are allowed to hold companies for longer periods when warranted; and the need for private equity managers to have products designed to tap the private wealth market.

For an example of how one firm is marketing its capabilities and experience, see a PDF from Partners Group, “Five lessons from 20+ years in evergreens.” Among the ideas it promotes are that an evergreen structure can allow for better adjustments to market environments (the differences in the type of investments it has made across time are striking); built-in vintage diversification (although the graphic in that section shows that there appears to be no holdings longer than that of a typical PE fund); and “more frequent and precise valuation assessments.”

Mutual funds in the crosshairs

It’s that time of the year, when mutual funds pay out capital gains distributions that cause taxable investors to pay up on gains realized by the funds they hold. Morningstar calculated preliminary estimates of those gains and published lists of the top fifty anticipated distributions in percentage terms (six are above 45% of net asset value) and by leading fund firms. There can be a variety of reasons for gains to occur beyond the normal decisions of portfolio managers, but one reason sticks out:

The common theme among most of these top 50 funds is outflows.

Whether triggered by a portfolio manager leaving or performance troubles, sizable outflows lead to bottom-line consequences for taxable investors (in addition to downward price pressure on any illiquid holdings during the fire sale).

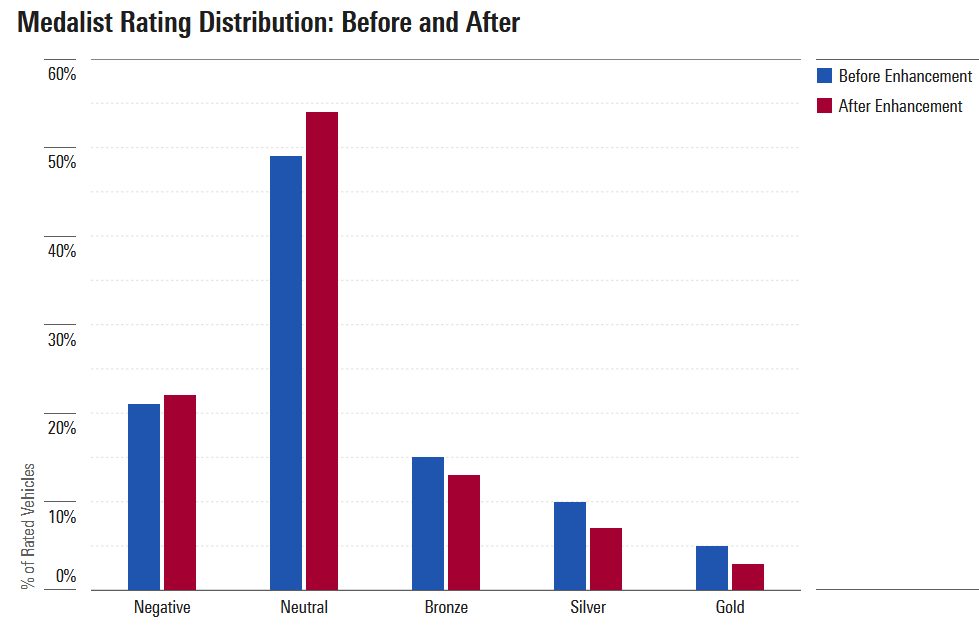

Morningstar also adjusted the methodology of its “medalist” rating system. As explained by Jeffrey Ptak (who had authored a note with additional information presaging the move), 12% of its 26,000 ratings were lowered as a result, versus only 3% that were raised. Equity funds took the brunt of it, with around 18% of them being knocked down at least a notch. Here are the distributions of ratings, before and after the change:

But that’s not the end of it. The medalist ratings are assigned in one of two ways, by analyst or by algorithm. Almost all of the initial moves were regarding algorithmic ratings; changes in analyst ratings will roll in during the coming months. The initial expectation is that a quarter of them will be altered — and that virtually all of those will be downgrades.

However, analyses of fund flows show that it’s not the medalist ratings from Morningstar that drive flows — it’s the famous star ratings that affect investor behavior. In that light, a recent research paper from Lauren Cohen, et al. (“Box Jumping: Portfolio Recompositions to Achieve Higher Morningstar Ratings”) is particularly interesting.

An important appeal of Morningstar’s [star] ratings is that they reflect the outcome of a standardized and transparent evaluation process largely based on pre-specified formulas. These features appeal to investors because the star ratings facilitate meaningful comparisons across several funds and avoid concerns over an ad hoc evaluation process. However, these same features of standardization and transparency make the rating system susceptible to strategic behavior and manipulation by funds, especially given the importance of higher ratings for fund managers in garnering fund flows and the corresponding revenues.

The authors show that purposely drifting into a nearby style box that has had lower returns can lead to increased flows because of the easier relative comparisons there, even though “funds appear to sacrifice [absolute] return performance when box jumping.”

Finally, a Financial Advisor IQ article points to a JPMorgan settlement that highlights the risks to a brokerage or RIA firm that puts its clients in mutual funds when (as is increasingly the case) a clone ETF is available.

Capital market assumptions

John Authers writes, “This is the season when investment houses publish their forecasts for the coming year, and I excoriate them as a waste of time.” But his target in the column that follows is that other annual ritual, the creation of long-term capital market assumptions:

In theory, very long-term projections should be driven more than anything else by the starting point. When stocks look historically expensive, expect the subsequent decade to be worse than the average, and vice versa. There are also sharply different ways to approach asset allocation, so you would expect a variation in approach. Instead, what emerges is: 1) remarkable stability in projections over time; 2) a tendency to herd around a few round numbers; and 3) an odd belief that some asset classes can do well regardless of circumstances — particularly private equity.

Authers offers a variety of supporting charts and concludes that “it’s disconcerting to see that even the institutions that really must plan a long way into the future are still so perfunctory in their long-term thinking.”

An ecosystem echo

Byrne Hobart’s article in The Diff, “The Modern Private Equity Business was Invented in Beverly Hills in the 70s,” has moved behind a paywall, but here are a couple of sections comparing today’s PE ecosystem with the one Michael Milken built at Drexel:

Put all of this together, and you have a suspiciously familiar financial ecosystem: there’s a central node that 1) has a good fundamental understanding of the businesses it’s involved in, 2) has essentially unlimited creativity for crafting new financial solutions if the old ones don’t work out, and 3) has enough of its own capital to own the highest-upside piece of every deal and enough captive outside capital to place all the paper that gets sold.

It’s also a model with natural conflicts. You have one party who’s well-informed, and who exercises more discretion than everyone else: clients do the best trades they can, but the very best ones are trades they won’t even see. Negotiating complex deals as both a principal and agent can leave plenty of profit for all sides when bid/ask spreads are wide, but the more asymmetric the information is, the longer those valuation gaps take to close. It’s a fantastically profitable approach, but it requires inputs: not just capital and talent, but an accumulated stock of either trust or owed favors that can be tapped at will. Counterparties know that they’re dealing with someone well-informed who aims to make a good profit from the transaction, and they’re willing to do this if they trust their counterparty to make the right moves. But this kind of leverage is hard to measure, and like other varieties it cuts both ways.

Other reads

“The king is dead, long live the king!” Rupak Ghose, Rupak’s Substack. It has gotten harder to be an active long-only bond manager.

“The art of being a lucky investor,” Simon Edelsten, Financial Times.

Do not target higher returns than markets seem likely to deliver — you will end up taking on too much risk to achieve them and only enhancing your likelihood of spectacular failure.

“What the future holds for quant investing: Ten hypotheses,” Mike Chen, Robeco. Including “faster model evolution and faster alpha decay.”

“How Asset Owners Are Redefining the Total Portfolio Approach,” Henry Fernandez, et al., MSCI.

Whatever approach a chief investment officer takes, fostering collaboration is job number one.

“Which Asset has the Best Bubble Potential?” Joe Wiggins, Behavioural Investment. The attributes that lead to a bubble, the classes of investors involved, and the distinction between fundamental assets and belief assets.

“Buybacks Gone Wrong: A Case for More Disciplined Capital Allocation in Corporate Finance,” Deiya Pernas, SSRN.

The root of this issue lies in the fact that most management teams lack a rigorous methodology for evaluating the intrinsic value of their company’s stock.

“Backdoor Private Credit Funds Are Luring Billions From Insurers,” Scott Carpenter, Bloomberg. “Rated feeders” allow insurers to cut their capital costs through “the alchemy of turning stakes in private debt funds into top-rated bonds.”

“When IR Met AI: How the Technology Is Shaping Earnings-Day Prep,” Mark Mauer, et al., Wall Street Journal.

Public companies frequently mention generative AI on earnings calls, citing its positive effect on the bottom line or promising results in tests. But there’s one application they leave unspoken: the technology’s role in those very calls.

“Green Bonds: New Label, Same Projects,” Pauline Lam and Jeffrey Wurgler, SSRN. The bonds “are usually not funding projects with green aspects that are particularly novel for the issuer.”

Turbulence

“A time of turbulence is a dangerous time, but its greatest danger is a temptation to deny reality.” — Peter Drucker.

Flashback: The subprime meltdown

We usually feature links from the past in this section, but this time we connect to a new story about the seminal financial crisis of this century. Doug Lucas runs the excellent Stories.Finance site, and this time the story is his own.

Lucas was a collateralized debt obligation (CDO) analyst for UBS at a time when those CDOs were stuffed with subprime mortgages. In the bloodbath to come, average write-downs were 55% for senior AAA-rated CDO tranches and 80% for junior AAA ones (with a median write-down of 100%!).

The tale is an amped-up version of the scrum that occurs whenever an investment idea with size and leverage and derivative vehicles gets taken too far. Those questioning the status quo are called names and accused of mounting a bear raid by those with a lot at stake; the experts (in this case the credit ratings agencies) make a stand by publicly defending their calls; and, on the other side, those who see calamity coming accuse the bearish of not being bearish enough. (Here, John Paulson was the accuser.)

In August 2007, before it all came tumbling down, Lucas was quoted as calling the subprime mess “The greatest ratings and credit risk-management failure ever.” Looking back now, of the lies involved in the mortgage originations “and the liars downstream” in the investment industry, he summarizes it all in this way: “One of the worse things humans have ever done to one another without using weapons of war.”

Postings

Almost two hundred postings are available in the archives, so try out some names and phrases in the search box and see what you can find. One example, “The Double-Edged Sword of Manager Selection,” includes this:

The expectation is that manager selection will take advantage of two edges, that of the manager and that of the selector. But, like the blades of a sword, each of those edges gets dull and chipped. They need to be honed to keep them sharp — although over time they can get so thin that they become ineffective. The sword as museum piece rather than as an advantage in battle.

Thank you for reading. Many happy total returns.

Published: November 25, 2024

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.