The most recent essay on the site deals with an important question for institutional asset owners (and other investors too). It is titled “Does it Matter (How the Money is Made)?”

Asset owners face dilemmas about whether the investment function ought to be an island unto itself, only concerned about the optimal risk/return profile for the portfolio, or whether other considerations ought to be factored into decision making.

Where do you stand on the examples that are given and how do you deal with the evergreen issues involved?

Emerging managers

The Yale Investment Office caused a stir with the announcement of its Prospect Fellowship initiative, a new emerging manager program. Ted Seides provides an excellent summary of the motivations and risks for Yale and for the managers who are selected, as well as the effects on other allocators.

Seides points out that, for Yale, which has had great success with emerging managers over time, “selecting a cohort of managers simultaneously is very different from investing opportunistically.” He also notes that “training them is not something Yale has done in the past.” In fact:

In a resource-constrained office, the time spent with applicants and Fellowship recipients may be better spent sourcing and working with managers in the rest of Yale’s portfolio.

Similarly, for those few managers that are among the tiny percentage of applicants who are selected, it’s likely that most of them ultimately will fail to make it into the core portfolio as they mature. Will they then “carry a Scarlet Letter of Yale’s rejection” that could prove costly in the marketplace?

The potential payoffs for those on both sides of the table in spite of those risks make this a program worth watching over the next many years. Seides provides a balanced view of the possibilities — and calls Yale’s program “a strong positive for the community of allocators,” since “the Yale imprimatur can help sway a governance board to adopt a similar program when that board might otherwise be overly concerned about risk.”

An investment process framework

A short transcript of a podcast features Mark Steed, CIO of the Arizona Public Safety Personnel Retirement System, and Ashby Monk of the Stanford Research Initiative on Long-Term Investing, who offer some simple ideas of profound importance.

Steed talks about the need for a disciplined approach to forecasting, saying that every investment recommendation should have three things:

One, you need a really clear definition of success. Two, you need a date by which you think success will be achieved or accomplished. And three, you need a probability estimate.

That approach is exceedingly rare within organizations and in interactions with external parties. Instead of clarity on those points, there is fuzziness. Almost no one speaks in specific probabilities, so there’s no way to keep track of how well forecasters assess the likelihood of events. On the contrary, there is lots of room to spin outcomes, which is unhealthy. As Monk remarks, “we revert to performance as our definition of a good decision,” even though that is a flawed approach.

Creating a “decision-friendly environment” ought to be the goal of every organization.

Measuring the moat

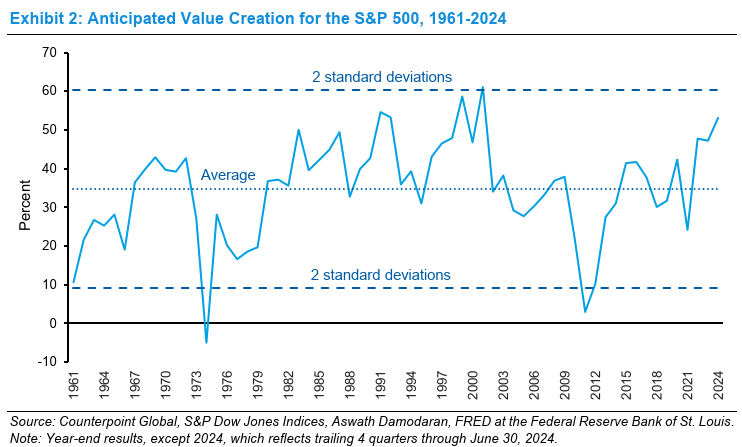

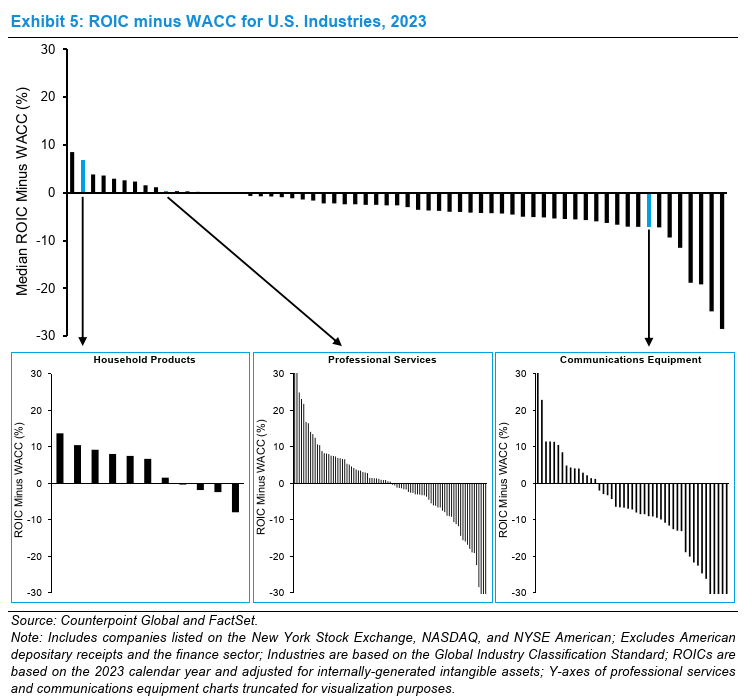

Michael Mauboussin and Dan Callahan have published previous versions of “Measuring the Moat,” the first of which appeared in 2002. The latest edition (subtitled “Assessing the Magnitude and Sustainability of Value Creation”) offers a broad perspective on the topic, including company life cycles; “the microeconomics of value creation;” industry structure and analysis; firm analysis; and much more. It is a crash course in equity analysis, complete with 47 exhibits. (See, for example, one that illustrates how ROIC minus WACC differs dramatically across industries and within industries too.)

{kind=link}

Since “the price of a company’s stock almost always anticipates future value creation”:

You can think of a stock price as having one part that reflects the value of the company operating at a steady state of profit and the other part that captures the value the company is expected to create or destroy with its future investments.

The exhibit above shows that the average anticipated value creation is about one-third of the price, but that it varies considerably over time.

Gender and analyst reports

A fascinating paper, “Gender and Analyst Reports,” by Bill Francis, et al., finds that:

Female analysts issue more readable reports and improve report readability over time relative to their male counterparts. However, female analyst reports are shorter, consistent with a “quality over quantity” approach. The textual sentiment of female analyst reports is also less optimistic, suggesting that they are more resistant to conflicts of interest than their male counterparts. In addition, we find that female analyst reports contain more nonfinancial content and are more long-term oriented.

While “men and women, as well as boys and girls, are more alike than they are different,” there are differences, and most every study regarding gender shows that women bring positive character traits into the male-dominated investment industry.

Fiduciary duty?

The chief executive of Focus Financial Partners offered a provocative point of view at an industry conference (as reported by Andrew Foerch for Citywire RIA):

If you’re not willing to take private equity or another form of capital, are you comfortable that you can fulfill your fiduciary obligations to your clients without it? These days, I think you have to ask yourself that question honestly and ask, you know, how?

Do you agree or disagree?

Other reads

“Rewiring The Financing Machine,” Larissa de Lima, et al., Oliver Wyman.

These changes must be considered holistically as they share a common underlying exposure — corporate credit. Different products vary in their liquidity and risk profiles, but innovation and competition are blurring the lines between products, complicating risk assessments and comparisons. Banks and various types of nonbanks are ever more interdependent, while nonbanks are becoming increasingly concentrated and diversified.

“A Private Equity Liquidity Squeeze By Any Other Name,” Michael Markov, CAIA Association. What if “the worst ever environment for liquidity” doesn’t improve soon?

“Jamie Dimon Is Right. Forget the ‘Damn Number’,” Jonathan Levin, Bloomberg.

As a general rule, many stock watchers spend too much time estimating earnings to the decimal point and too little digging into the ways that their thesis may be wrong.

“Fund Family Digest: US in 2024,” Bridget Hughes, Morningstar. Only ten of the largest 150 mutual fund firms receive the highest “parent” ratings (“how well an asset manager stewards capital in the best interests of its investors”) from Morningstar. An overview of key indicators is provided for each fund firm.

“Tech boom forces US funds to dump shares to avoid breach of tax rules,” Nicholas Megaw and Will Schmitt, Financial Times.

The need to reshuffle holdings could drag on fund performance and trigger capital gains taxes.

“A complicated way to do something very simple,” Joachim Klement, Klement on Investing.

But if volatility targeting funds in the equity space is simply a complex way to exploit trend following, why bother with the higher fees charged by these products?

“Timeless principles of board dynamics,” Bob Rosone and Maureen Bujno, Harvard Law School Forum on Corporate Governance. A set of basics for governing bodies, including investment committees.

“Watch Out: Wall Street Is Finding New Ways to Slice and Dice Loans,” Matt Wirz, Wall Street Journal.

Wall Street is cranking up its complex bond machine again.

Always

“The wave of the future is coming and there is no fighting it.” — Anne Morrow Lindbergh.

Flashback: The machine

In 1984, Barton Biggs wrote a strategy piece for Morgan Stanley, “The Giant Present Value Machine Downtown.” He quoted Jim Harpel, who had “an honorary PhD in net worth enhancement from the financial markets, the premier graduate school in the world,” as referring to the stock market as “nothing but a giant present value machine.”

Biggs stated his objections to the thought that there’s a simple function that connects the stock market to the bond market, questioning assumptions about the equity risk premium and noting that the present value machine “can’t factor in qualitative factors and secular change.”

While the topic is relevant today, the specific references are a bit quaint. Biggs debated whether the “justifiable price/earnings ratio” should be ten or thirteen (!), and it’s worth noting that the machine is no longer thought of as being downtown.

He concluded by writing of the great John Templeton that he “is unmoved by valuation and so am I.” Forty years on, one wonders what the two would think of today’s environment.

Postings

Past editions of the Fortnightly can be found in the archives, as can all of the original essays on a variety of topics. For example, “Questions about the Dominance of Indexed Strategies,” which explores a number of dimensions about the changes in market structure and behavior from indexation (of broad-based passive exposures, as well as other strategies):

Taken as a group, indexed strategies are definitely popular — hugely popular. If the “price pressure hypothesis” is valid at all, the size of the asset pool and the enormity of the ongoing flows pose important questions for participants in all corners of the ecosystem.

It was published in 2022. The series of questions posed in the piece are even more relevant today.

Thank you for reading. Many happy total returns.

Published: October 28, 2024

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.