If you find these Fortnightly linkfests of value, please subscribe and encourage your coworkers and friends to do so too. Word of mouth is the most powerful marketing tool for the writing and services of The Investment Ecosystem.

Upcoming postings include one about the game of speed in the investment world (as well as within organizations) — and another on some difficult choices for asset owners.

On autopilot

“Target” is a loaded word. In most cases, it’s used in a promotional way, with the intent to anchor expectations. And it often works. See, for example, how the target IRR advertised by a general partner makes its way into an asset owner’s investment memo — or how a target volatility can narrow expectations in ways that fit with the current market regime but minimize the broader possibilities of other days.

And then there are target prices issued by equity analysts, often a vehicle for hype. Those targets are the subject of a paper by Itzhak Ben-David and Alex Chinco. They contrast the academic expectation — that analysts would apply present-value logic to the calculation of a target price — with the fact that analysts instead overwhelmingly use the simple formula of the title, “Expected EPS × Trailing P/E.”

Analysts are required to show within their research reports how they came up with their target prices. In studying a collection of reports, the authors find that multiples rule the day, dominating the use of discounted cash flow methods to determine target prices. And:

When analysts do use a discount model, they often implement it in a way that is inconsistent with present-value reasoning.

There is a notable divide between theory and practice:

Financial economists think about the discount rate embedded in this pricing rule as the most important part of the problem. By contrast, the analysts in our sample focus all their attention on predicting a company’s earnings. They pick a recent P/E almost as an afterthought.

The authors acknowledge that “every profession does some things on autopilot.” That’s why examining embedded assumptions and existing practices should be a regular routine. Why are things as they are and do opportunities exist if you look at them differently?

Battle lines

The promoters of private equity and its doubters are like the two ends of the political spectrum, each hardening their positions, even as the environment for the strategies has changed measurably over the last few years.

On the “pro” side, Ted Seides wrote a posting in which he quoted David Swensen as saying that private equity is “a superior form of capitalism,” and offered a section that is a “rebuttal to common critiques of private equity.” As is common, Seides references the “long-term capital” that private equity managers have to put to work, while later writing that “the average holding period is three to five years.” That disconnect contributes to the abuses and failings of the model, something perpetual or multi-decade fund structures attempt to address.

Among those taking the other side is Jared Dillon, who penned a paper called “The Next Big Short: Hidden Risks Behind Private Equity’s $8 Trillion Market”:

If you are going to a restaurant, a car wash, or a dentist’s office, there is a good chance that it is owned by private equity.

And you have probably noticed that service has deteriorated, and prices have increased.

The reason is that there is a mismatch in priorities between the founder of a business and the private equity owner of a business. The founder of a business thinks long-term: How do I please customers and keep them coming back? A private equity owner only thinks about short-term profitability: How do I extract the most value out of each customer and transaction?

As the title indicates, Dillon tries to draw parallels between the rapid growth in private equity (and private credit too) and that of the mortgage market before the financial crisis — noting some cracks that have appeared and giving a warning: “If things really start to break, it could trigger a cascade of effects across the financial system.”

(In the category of historical evidence — which may or may not be worth relying on given the considerable changes in the competitive and economic environments — in July, Dimensional Fund Advisors released a paper, “Understanding Private Fund Performance,” as well as a shorter summary of the findings.)

Investing considerations

Vanguard issued a pair of basic guides for clients: “Considerations for index fund investing” and “Considerations for active fund investing.” Links to them and other related materials (including a piece on combining active managers in a portfolio) may be found here, where the simple frameworks for index and active investing are compared.

The above illustration comes from the active report. The simple visual gets at an essential element of active investing — that there is an expectation of outperformance that makes the chore harder. (Our due diligence course stresses the importance of identifying the outperformance goal and an assessment of the probability of reaching it over an extended period of time — in advance of making a commitment.)

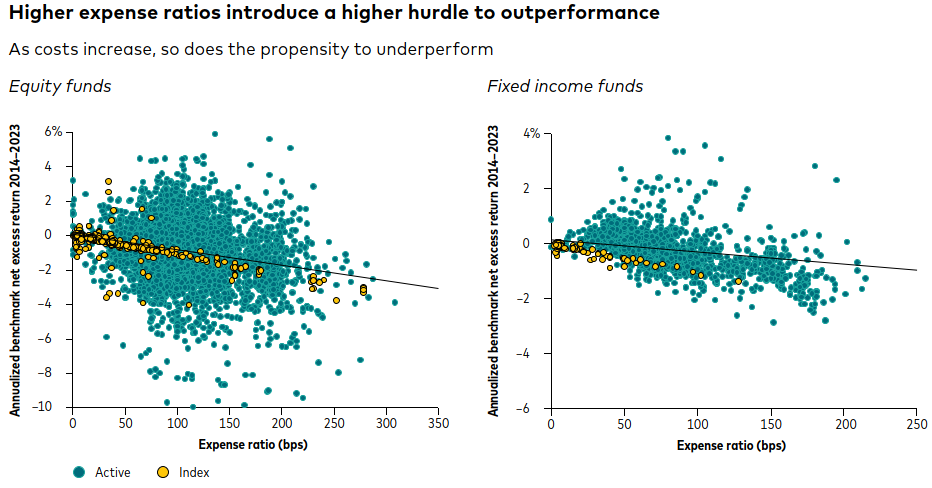

Of course, paying higher fees makes it harder to achieve benchmark returns, to say nothing of benchmark-plus ones. To wit:

In general, the higher the fees the less likely mutual fund investors will outperform.

Other reads

“Private Credit’s Next Act, Huw van Steenis, et al., OliverWyman.

The need to secure access to these new asset classes is prompting private credit players to change tack, looking to partner up with banks rather than be their adversaries.

“The Power of Expectations: Nvidia’s Earnings and the Market Reaction!” Aswath Damodaran, Musings on Markets. The “dance between companies and investors, playing out in expected and actual earnings.”

“Distress Investing: Crime Scene Investigation,” Sebastien Canderle, Enterprising Investor.

The widespread overcapitalization of start-ups and quasi-universal overleveraging of buyouts have led to a deep-seated zombification of private markets.

“It’s time to end creditor-on-creditor violence in sovereign restructurings,” Jay Newman, et al., Financial Times.

Why have some of the world’s most sophisticated institutions and investment firms allowed themselves to be co-opted and drawn into a process that relegates them to supplicancy?

“In Praise of High-Volatility Alternatives,” Cliff Asness, AQR. Are compound returns overrated at the line-item level?

“What we see when we look at price charts,” Joachim Klement, Klement on Investing.

It turns out that people who focus more on the most recent data points tend to make more trend-following, momentum-driven forecasts, while people who take in the whole price history tend to be more contrarian in their forecasts.

“Bonds Behaving Badly,” Kathryn Kaminski and Jiashu Sun, AlphaSimplex. One section is titled, “Inflation Changes How Asset Classes Behave,” which includes a conditional distribution of bond returns and volatility across different inflation regimes.

“Steer clear of the accountability sink,” Simon Evan-Cook, Citywire Selector.

The industry is now riddled with accountability sinks: combinations of rules, committees, decision-making structures and procedures that mean no individual is responsible when the machine does something stupid.

“The Risk and Reward of Investing,” Ronald Doeswijk and Laurens Swinkels, SSRN. A new look at the results of the “global market portfolio” (which excludes “emotional assets” and private vehicles for which market prices are not available).

“Beware of Sharpe Objects,” Tommi Johnsen and Preston McSwain, Fiduciary Wealth Partners.

Even though it is common to see investment advisers compare the Sharpe Ratios of investment funds inside a portfolio to one another, it was not intended to be used this way.

“Watching the Watchdogs: Tracking SEC Inquiries using Geolocation Data,” William Gerken, et al., SSRN. An eye-opening example of how data is stitched together these days. What else like this is out there?

Wasted time

“The man who views the world at 50 the same as he did at 20 has wasted 30 years of his life.” — Muhammad Ali.

Flashback: Hedge fund time capsule

In late 1996, Ted Caldwell of Lookout Mountain Hedge Fund Review offered a “Time Capsule Opinion.” The issue asked (and answered) the question, “If you were to lock up your money in one hedge fund for the next ten years, which one would it be?” Caldwell wrote of the difficulty of the task, admitting:

Luck has historically dwarfed brilliance in the early selection of the phenomenal money managers.

He added:

The science of investing ponders the past, while the art of investing focuses on the future.

The piece contrasts a conservative Jones model fund from an aggressive one — and notes that many successful funds started as the former (and “gained most of their performance” from it, even if that foundation “has been concealed for some time under layers of more sensational strategies”). Of course, today’s hedge fund environment is much changed, with a multiplicity of strategies and business models.

Caldwell’s lockup pick in 1996 was Lee Ainslie’s Maverick Capital. According to a 2007 article from Institutional Investor, Maverick indeed had good returns in the first part of the ensuing decade before struggling in the last few years of it. (The article referred to Ainslie as the “Comeback Kid” based on a strong 2007, which was helped in part by shorting some subprime mortgage lenders in advance of the financial crisis.)

Postings

As seen in the flashback sections of each Fortnightly, around here we like to look back for lessons from both well-known and obscure events of the past. One example is a posting published in 2021, “Enron: Bad Bets and Surprising Outcomes.” It ends:

Narratives can overpower analysis (and ethics). “Vigilance and skepticism” can be viewed as hindrances to the game as it is played, instead of being recognized as essential qualities for good work.

All of the previous postings can be found in the archives.

Thank you for reading. Many happy total returns.

Published: September 16, 2024

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.