A couple of new essays will be up on the site in coming days. One looks at the need to assess the provenance of a firm’s investment approach (including claims of authenticity), and the other peeks behind the narrative curtain of a famous asset management firm. (If you’d like to receive postings via email as they are published, you may subscribe here.)

On to the readings.

The misunderstood and unpopular

Brent Beshore’s annual letter about Permanent Equity contains updates on the firm (which buys private companies in thirty-year funds) and some personal reflections from Beshore.

Of particular interest is a section titled “Culture of Buying the Misunderstood.” It highlights a widespread issue throughout the investment world (public and private):

From the associate to the VP to the MD to the investment committee to the diligence team and the bankers, there’s a decreasing ability to spend time on the investment, decreasing risk tolerance, and escalating career risk, which creates an ever-increasing need to have the investment look good and be easily understandable.

The more I get into institutional capital markets, the more I realize it’s one big career-risk, principal-agent problem from bottom to top across LPs and GPs.

Beshore writes that “all businesses are loosely functioning disasters,” reflective of the Investment Ecosystem mantra that “all organizations are messy.” Permanent Equity seeks to avoid the career-risk playbook and “to remain open to the weird, the ‘furry,’ and the complicated, and to create a culture that rewards taking idiosyncratic risks.”

(An echo of that in the public markets comes from Eric Cinnamond of Palm Valley Capital Management in a posting, “The Art of Looking Stupid.” Of standing apart from convention, he says, “Instead of being embarrassed, we view our ability and willingness to look stupid as a competitive advantage.”)

Knowing a person

“How to Know an Investment Manager” is a recent piece from the pseudonymous ECAllocator. The author recommends How to Know a Person by David Brooks as a valuable book for those who allocate capital. Here’s why:

Do most allocators actually dig into people sufficiently to really know the person(s) they are about to allocate significant capital to, and have convictions that they possess what the allocators “likes”?

I believe the answer to be no.

While meeting managers is viewed as a critical part of the selection process, few have been trained in the art of interviewing. (For starters, as the author reminds us, “The interview isn’t about you.”) Importantly, the distinction should be drawn between interviewing and conversation. They are different from each other yet offer complementary avenues for discovery, “so you can really understand a manager, and why they possess the characteristics you think are important.”

Easy money

In his latest memo, Howard Marks of Oaktree walks through the effects of low interest rates. He uses the analogy of “the moving walkway at the airport”:

If you walk while on it, you move ahead faster than you would on solid ground. But you mustn’t attribute this rapid pace to your physical fitness and overlook the contribution from the walkway.

Easy money encourages not just a distorted view of one’s capabilities, but risk taking and the loosening of investment standards:

I love Hayek’s word “malinvestment,” because of the validity of the idea behind it: in low-return times, investments are made that shouldn’t be made; buildings are built that shouldn’t be built; and risks are borne that shouldn’t be borne. . . . The investment process becomes all about flexibility and aggressiveness, rather than thorough diligence, high standards, and appropriate risk aversion.

Marks extensively quotes The Price of Time, a book by Edward Chancellor, including:

The Manchester banker John Mills commented perceptively [in 1865] that “as a rule, panics do not destroy capital; they merely reveal the extent to which it has previously been destroyed by its betrayal into hopelessly unproductive works.”

We are in a time of wishful thinking, as investors argue for a return to the low rates that has framed recent experience, but Marks pushes back on the consensus:

My answer is that today’s rates aren’t high. They’re higher than we’ve seen in 20 years, but they’re not high in the absolute or relative to history.

The impact of rates

Jesse Livermore and Ehren Stanhope produced a report for the Canvas platform of O’Shaughnessy Asset Management called “Climbing the Maturity Wall of Worry.” The subtitle, “Interest Expense as a Source of Earnings Risk for the U.S. Equity Market,” states the authors’ goal of identifying the bottom-line impact if rates stay where they are.

The report is full of exhibits, including ones that show the dramatic changes in margins and interest rates over the last sixty years. The conclusion of the analysis is that the effect on earnings in a flat interest rate environment will be “small to moderate” for large firms but more consequential for lower capitalization stocks and for some sectors (especially real estate).

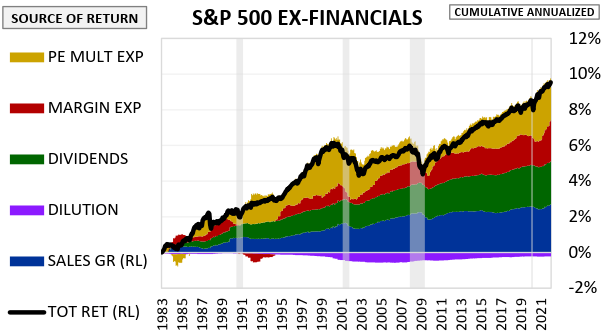

The chart above needs a bit of explanation. At every point across time, it shows the cumulative real return to date, annualized using the entire time frame of the analysis. That way it’s easy to see how the different components of return aggregate over time.

It’s quite remarkable that the four main components — sales growth, dividends, margin expansion, and multiple expansion — were so close together in impact, with each one contributing between 2.31% and 2.69% to the aggregate real return of 9.54%.

Different strokes

One of the biggest stories of late is the vote by the SEC to allow the trading of bitcoin ETFs. John Rekenthaler of Morningstar wrote a column saying that “Vanguard Got Bitcoin Right” because it did not create a bitcoin ETF and does not allow trading of any of those that exist on its brokerage platform.

Rekenthaler praised Vanguard’s mindset, detailing a handful of the can’t-miss products over the years that the firm steered clear of that went on to “crash and burn.”

Franklin Templeton took the opposite approach from Vanguard, introducing a bitcoin product and adding laser eyes (a pro-bitcoin indicator for avatars) to the face of long-time corporate symbol Benjamin Franklin, who was known for his thriftiness. The firm’s social media blitz included a tweet, “In crypto, speculation is a feature, not a bug.” (See FT Alphaville’s take on it all.)

Unfortunately for Franklin Templeton, in a crowded field the flows into its bitcoin ETF have been almost nonexistent since its debut.

Other reads

Unpacking Private Equity Performance, Gregory Brown and William Volckmann, SSRN.

Our analysis shows that intermediate and final IRR are strongly affected by subscription line maturity, and intermediate IRR is significantly affected by deployment pacing. Intermediate and final MOIC are strongly affected by recycle deal accounting methodology, and intermediate MOIC is strongly affected by deployment pacing and subscription line maturity. Consequently, LPs need to be very cognizant of these issues when measuring and utilizing fund performance measures.

“Superstar Brands,” Kai Wu, Sparkline Capital. Using trademark yields, trending product yields, and search interest yields to identify firms with brand portfolios that are undervalued by the market.

“Vintage Voodoo,” Stephen Nesbitt, Cliffwater.

Vintage year has played an important role in the traditional playbook for private asset investing. This is a mistake, both when allocators target specific vintages opportunistically and when they purposefully parse commitments across multiple vintages in the name of diversification.

“The Puritans of Venture Capital,” Kyle Harrison, Investing 101. A short history of VC, including the split into camps of “cottage keepers” and “capital agglomerators.”

“ESG Skill of Mutual Fund Managers,” Marco Ceccarelli, SSRN.

We differentiate between proactive managers, whose trades predict future changes in ESG ratings, and reactive managers, who change their portfolio allocation after a change in ESG ratings occurs.

“Out with the Old and in with the New: a 50% Private Markets Portfolio,” Ares, InvestmentNews. In which a private asset manager uses sponsored content in a publication for investment advisors to argue that “a 50% allocation to private markets” is optimal.

“Too Good to Be True,” Christopher Schelling, LinkedIn.

It may sound simple, but starting from a position of no to everything makes a huge difference. While I don’t think it’s productive to begin a professional relationship from a position of distrust, blind trust should never be presumed in this industry. The old adage “trust, but verify” gets it backwards, I’m afraid.

“The Industry Needs Innovation. Could the ETF’s Story Be a Template?” Angelo Calvello, Institutional Investor. A history lesson to inform the innovation “that our industry so desperately needs.”

“Large Backers of Private Equity Are Asking For Their Money Back,” Laura Benitez, et. al, Bloomberg.

“We’re now undergoing a real cultural change,” said William Barrett, managing partner at Reach Capital, a private-market fundraising firm. “It’s the first time we’re seeing LPs being so straightforward and linking a distribution from one fund to a new commitment in another.”

Character

“Any fellow who will cheat for you will cheat against you.” — Sam Rayburn.

Postings

Thank you for reading and passing this on to others.

Check out the archives, where you’ll find other editions of these curated readings, as well as in-depth looks at ideas and developments of interest to investment professionals and organizations who want to stay in the forefront of changes happening across the industry.

Many happy total returns.

Published: January 22, 2024

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.