“Every organization faces the same dilemma, over and over: how much to stay the same and how much to change.” That’s the start of the most recent posting on the site, “Balancing Exploration and Exploitation in Investment Organizations,” which provides frameworks and ideas for you to use in considering whether your organization’s current balance is appropriate.

If you haven’t subscribed to receive emails of the postings, you can do so here. Then you won’t miss any future editions of this Fortnightly — or the more in-depth essays about the investment world.

Creating effective investment committees will be one of the upcoming topics. That means different things depending on the type of organization involved. What are the challenges you face in that regard? Please share your thoughts.

What the job is

An eFinancialCareers posting from September referenced an Invest Like the Best podcast featuring Will England of Walleye Capital. England was quoted as saying that it’s hard to find portfolio managers for the firm’s multi-strategy fund. Not because of a lack of investment talent, but because they need to be able to handle the psychological pressures involved:

The job of being a PM, whether you’re quantitative or fundamental, is psychologically extremely toxic because you’re going to be wrong basically just as much as you’re going to be right. You’re going to get kicked in the face a lot, and you’re going to be someone who’s the smartest person that they’ve known their entire life, and then they’re just going to get beat up all the time.

That toxicity, said England, is “what the job is.”

Which begs the question in a headline for a Citywire Selector interview with David Roberts, a long-time fixed income manager, “Do fund managers get enough support with mental health?” While jobs at traditional fund companies might not be as toxic as those at hedge funds, there are pressures — and when you’re the perceived expert (even “star”) who is supposed to project confidence, it can be hard to seek help. Most investment cultures are competitive, not supportive, so where would you go anyway?

The closing comment from interviewer William Robins, regarding the benefits of managers commiserating with each other, is: “You are humans, after all.”

Defined benefit investing

Investors come to the markets with different goals, mandates, and restrictions, which affect the choices that they make. Defined benefit pension plans are a good case in point, since their concerns vary from those of many other investors. A report from Mercer offers recommendations in four areas.

The first is “journey planning,” or “how the plan will be managed to its ultimate destination” given the rules that govern the payment of the liabilities over time. Several different metrics come into play to map out the best path for investing to meet the liabilities depending on the funding status of the plan and whether it is slated to be terminated at some point in the future or run indefinitely (and what options exist if the plan is in surplus).

The second section considers how investment strategies are a function of that funded status and how they have been affected by recent market changes. The report repeatedly emphasizes how private assets can reduce funded status volatility, a striking example of the ways in which the popularity of such strategies has been driven by the performance smoothing that masks the real underlying economic variability of the assets.

The last two parts deal with liability hedging and governance issues.

Rethinking due diligence

A number of BIPOC asset managers are advocating “due diligence 2.0” in response to industry practices that make it difficult for diverse managers to gain a foothold.

A list of nine recommended shifts in due diligence processes provides a good discussion framework about beliefs and current practices. For example, do we think about track records or assets under management in ways that make sense, or are we just adhering to convention?

The posting includes the asset allocators, advisors, and asset owners who have so far made a commitment to the set of principles.

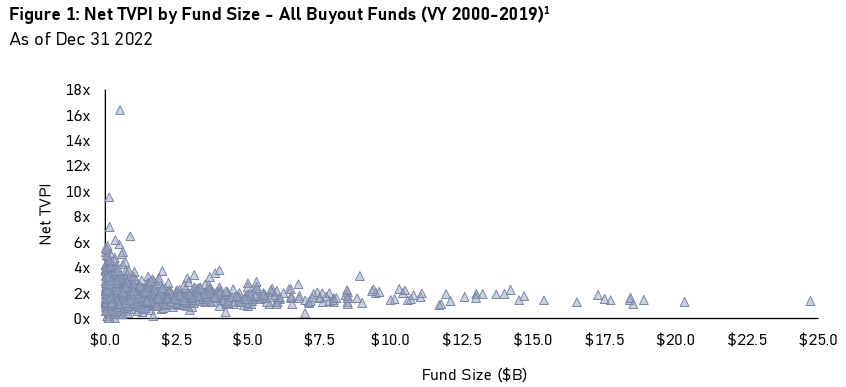

Small buyout funds

Abbott Capital creates and manages private equity programs, so it’s not surprising that a report it published, “Do Small Buyout Funds Still Belong in a Diversified Private Equity Portfolio?” answers the question with a “yes.”

The image above, charting net total value to paid-in capital by fund size, illustrates the rationale in terms of historical performance, which is further demonstrated in additional exhibits. The focus is on the greater upside potential of smaller funds, although, “Left tail risk, that is, underperformance or loss of capital, appears more common with small funds.”

The report covers the challenges of smaller funds for allocators at opposite ends of the spectrum. Those with a sizable private equity portfolio often find that given “the velocity at which they need to deploy capital . . . the small buyout market is too inefficient.” Conversely, those without sufficient resources can be overwhelmed by the sheer number of small funds that have proliferated in the face of time and expertise limitations.

More important is a short section on the “why” of historical outperformance of smaller funds, which sketches out the attributes of the purchased businesses that make entry multiples lower than those for larger firms and allow for substantial improvements in results.

Also see “Proving Persistence,” an analysis from Andrés Ramos and Patrick Coleman of Nasdaq. They use the eVestment database to examine the persistence of TVPI and IRR in subsequent funds as they grow in size.

AI concerns

Along with many articles on the promise of AI in investment decision making, operations, and marketing, there are concerns. For instance, “Will AI Compromise Security for Institutional Investors?” is an article by Danielle Walker in Chief Investment Officer. It deals with a range of specific issues, as well as the implications of the SEC’s proposed rules regarding the use of AI applications.

The rules will apply to many different types of firms, including those providing financial advisory services. On Nerd’s Eye View, Ben Henry-Moreland offers perspective on the implementation issues for advisory firms, including, as one section header says, “using technology as a fiduciary means knowing how it works.”

Other reads

“Fifty Shades of Grey Swans: Timeless Risks with a Modern Twist,” Matt Tracey, Alpha Architect. Ideas about dealing with uncertainty — and two lists of questions to evaluate your readiness for different environments and situations.

“Risk Parity Not Performing? Blame the Weather,” Markov Processes.

A less highlighted casualty of the changing stock/bond relationship, however, has been risk parity — and the pension funds that adopted such institutional-oriented strategies and products en masse.

“My Top Stock and Fund Picks for 2024, Joe Wiggins, Behavioural Investment. “Such guidance is good for commissions and clicks, but bad for investors.”

“How Tokenization Can Fuel a $400 Billion Opportunity in Distributing Alternative Investments to Individuals,” Tyrone Lobban, et. al, Bain.

Tokenization has the potential to change how alternatives work by making it easier to distribute and invest in funds and adding investor-friendly features to help bridge the gap between alternatives managers and individuals.

“SBCERA’s Recent Outperformance: A Tale of Two Benchmarks,” Brian Schroeder, CAIA Association. Using both broad-static and specific-dynamic benchmarks together can be an “insightful combination” for understanding asset owner performance; but looking at just a broad-dynamic policy index muddies the water.

“Is private credit a systemic risk?” Robin Wigglesworth, Financial Times.

But investors losing boatloads of money is not the same as a financial crisis. In fact, trillions of dollars can evaporate, prominent investment funds be forced to gate and major financial institutions can go belly-up without a wider conflagration, as long as policymakers douse the flames rather than fan them. Viz 2022-23. Not everything is a “Lehman moment.”

“The Math of the Multi-Manager,” Brian Hurst, ClearAlpha Technologies.

The success of the multi-manager model depends less on accurately forecasting individual portfolio managers’ performance and more on reaping the advantages of diversification by implementing numerous, mostly independent strategies simultaneously.

“Bobby Jain Slashes Fees to Draw Clients Before Hedge Fund Debut,” Nishant Kumar and Hema Parmar, Bloomberg. Why is the hottest new fund in years (at least according to reporting over many months) cutting fees again in advance of its launch?

“Burned Investors Ask ‘Where Were the Auditors?’ A Court Says ‘Who Cares?’ ” Jonathan Weil, Wall Street Journal.

One of the country’s most influential courts has asked the nation’s top securities for its views on an uncomfortable subject: whether audit reports by outside accounting firms actually matter.

“Future Fund CIO rejects ‘macho, Darwinian’ investing culture,” Aleks Vickovich, Top1000funds.

History and life teach us that there is far more to life than conflict. We spend far more time creating, collaborating, interacting constructively, and pursuing our passions and our curiosity than we do fighting.

Are you listening?

“Formulating an opinion is not listening. Neither is preparing a response, or defending our position or attacking another’s. To listen impatiently is to hear nothing at all.” — Rick Rubin.

Flashback: Think for yourself

Adams, Harkness & Hill was a Boston-based firm that specialized in covering technology, health care, and consumer stocks. Oakes Spalding started the firm’s 100 Emerging Growth Stocks product.

In a 1984 report, he wrote:

I am a brokerage house analyst who has, I am told, some influence. I have been in this business long enough to have become very cynical about its goings on. I hope to become even more cynical and benefit thereby. But it is humbling to contemplate the power that I and other “Street-side” analysts now have — power we do not deserve, but that we have because a large part of the market finds it easier to lean on our every word rather than think for itself.

Quite an uncommon thing for an analyst to say.

Postings

Thanks for reading. Check out the archives to see all of the latest content — and things further back, like “Reviewing the Asness Peeves,” a posting that reviews a well-known Cliff Asness commentary (and asks what “things said or done in our industry or said about our industry” bug you).

Thanks for reading. Many happy total returns.

Published: January 8, 2024

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.