The most recent essay on the site was “Identifying Unrealistic Expectations in Manager Selection.” One technique — using a straightforward question, regularly asked — can frame a current analysis and improve the entire selection process over time.

On to the readings as we prepare to enter 2024.

Pattern recognition

The latest report from Michael Mauboussin and Dan Callahan looks at the “opportunities and limits” of pattern recognition:

Investors and investment organizations regularly cite pattern recognition as the basis for action. While it can be extremely powerful and useful when applied appropriately, it can also be highly misleading and furnish fuel for overconfidence when used inappropriately.

Unfortunately for us, markets represent “wicked” rather than “kind” environments, rendering useful pattern recognition less likely than in many other pursuits. While investment professionals are usually expected to (and expect to) opine on what will happen going forward, the landscape is full of landmines that can blow up narratives and actions.

The report offers a multi-dimensional perspective on pattern recognition and ideas to improve the process. Reminding ourselves of the challenge is a good start, otherwise we are prone to remember the times when we saw patterns and capitalized on them for good effect — and to forget the times when they were illusory or misleading.

Category fraud

Evan Frazier of Marquette Associates offered a posting that asked the question “Is China Guilty of Category Fraud?” The question is not really about China, but about MSCI’s treatment of it within its index family. There are always examples of questionable categorization to be found, presenting choices about playing against an index or popular approach versus what seems right given an investment mandate. Categories and distinctions are constantly in flux, with capital flowing as a result, so staying ahead of that sense-framing is an underappreciated part of active management.

New foundations

The sloppy fundraising environment in many area of private investment has intensified the interest of fund purveyors in targeting advisory firms where penetration is small. Take as examples reports from KKR (“A New Foundation for Global Wealth”) and the Defined Contribution Alternatives Association (“Considering Private Real Estate as a Foundation of DC Plan Multi-Asset Options”). The pitches include references to past performance (with smoothing) that may or may not be good indicators of future outcomes. How solid will such promised foundations be?

Return assumptions

We’re now in the heart of the returns expectations season, as firms announce their predictions for the coming year and further out.

Of course, no one knows what the future will bring and single-point estimates don’t really provide any useful information, despite the headlines they generate. But the underlying assumptions can be revealing as to mapping out the possibilities.

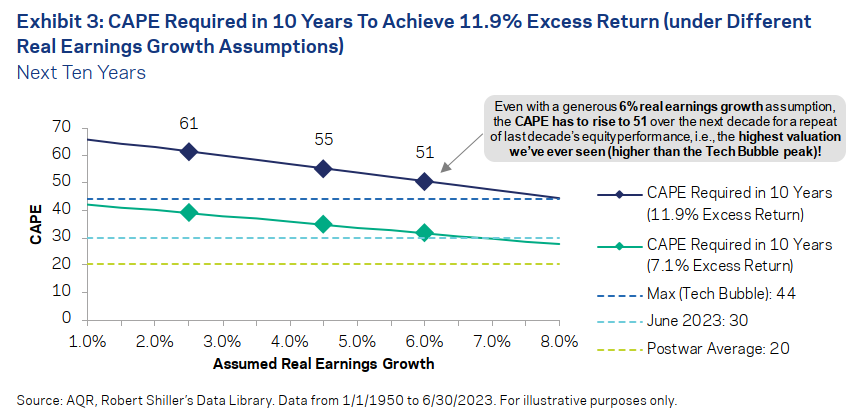

Along those lines, Jordan Brooks of AQR penned a report, “Driving with the Rear-View Mirror,” which looks at the elements of equity returns (Excess of cash return = Dividend yield + Real earnings growth + Multiple expansion – Real cash return), to answer the question, “Will we see a repeat of the past decade of U.S. equity returns?”

One of the illustrations, shown above, is a good starting point, although advocates of an AI-induced boom would argue for the X-axis to include higher numbers to the right.

Other reads

“The Difference Makers: Key Person(s) Valuation,” Aswath Damodaran, Musings on Markets.

Intrinsic value is built, not on nostalgia or emotion, but on the cold realities that key people can sometimes destroy value, that a key person in a company can go from being a value creator to a value destroyer over time and that key people, in particular, and human capital, in general, will matter less in some companies (more mature, manufacturing and with long-standing competitive advantages) than in other companies (younger, service-oriented and with transitory and changing moats).

“Interviewer vs. Criminal Lawyer,” Chenmark. What makes for a good meeting when you are interviewing someone?

“The Rise of GP Seeding as an Institutional Asset Class,” GCM Grosvenor.

Seed and stakes investors recognize an opportunity to participate as minority owners in stable and predictable cash flows across management fees, carried interest, and balance sheet investments over a long duration.

“To Roll or Not to Roll (Forward): LP NAV Estimation for Private Equity and Real Estate,” Aili Chen, PGIM. “For CIOs who wish to follow a consistent LP estimation approach over time, we measured cumulative estimation errors over multiple quarters.”

“What I have learnt in 37 years of financial journalism,” Jonathan Guthrie, Financial Times. Among the lessons:

Individual incentives favour collective instability.

You do not hear the whistle of the bullet that hits you.

Stock analysts are hedgehogs not foxes.

Debt matters more than equity, unfortunately.

“Exploring Relevancy in the Family Office,” Fidelity. A look at the relationships that are critical to creating a successful family office (and the potential pitfalls); a list of “questions executives and families should ask of themselves” is included.

“A View into New York City CRE Market Distress,” Maverick Real Estate Partners. This look at lending in premier commercial real estate market is full of interesting illustrations.

“See the S&P 500 From a New Lens,” Paul Kenney, Syntax.

Our Know What You Own series focuses on helping investors understand the business risks embedded in commonly used benchmarks, including the quantification of themes like technology and real assets that cut across sectors.

“These Boards Are Meant to Protect PE Investors. Why Can’t Anyone Agree on How?” Alicia McElhaney, Institutional Investor. An overview of some of the issues involved with limited partner advisory committees (LPACs), including, “The allocators on an LPAC have no fiduciary duty to other allocators in the fund.”

“Byrne Hobart, the unlikely oracle,” Shreeda Segan, Meridian. A profile of the prolific and influential newsletter author (including a link to his 2017 posting, “How I Got Hired at SAC Capital Without a College Degree”).

“GPT and other AI models can’t analyze an SEC filing, researchers find,” Kif Leswing, CNBC.

“There just is no margin for error that’s acceptable, because, especially in regulated industries, even if the model gets the answer wrong 1 out of 20 times, that’s still not high enough accuracy,” Qian said. [Rebecca Qian of Patronus AI.]

“Multi-manager risks & a buyside network topology,” @stwill1. A thread exploring the dynamics of the pod shops and some implications.

Still learning

“Ancora imparo.” — Michelangelo. (This quote, meaning “I am still learning,” was supposedly said by the great artist in his late eighties, although some dispute it. If he didn’t say it, he could have, since he continued to create until his death in 1564.)

Flashback: Equity Funding

According to Howard Schilit in Financial Shenanigans, Equity Funding Corporation of America “began operations in 1960 with $10,000. By 1973, the company purported to manage asset of $1 billion.” But it was a fraud.

Raymond Dirks, a Wall Street analyst, received information to that effect, informed a Wall Street Journal reporter, and told his clients to sell the stock. The company collapsed and some of its officers went to prison, but in the aftermath, Dirks became the most high-profile analyst on the Street and investment organizations would modify their compliance practices as a result of the ensuing debate.

Dirks was censured by the S.E.C. for violating insider trading rules, an action which he fought for a decade before the Supreme Court overturned it. The New York Times obituary for Dirks, who died this month, quoted Justice Lewis Powell as saying the S.E.C.’s interpretation threatened “to impair private initiative in uncovering violation of the law.”

Postings

Removing the paywall on the site has opened up 150+ articles in the archives focused on the continuous improvement of investment organizations.

One example is “It’s The Political Season (Always).” Four short items about political beliefs and how they affect investment decision making.

Thanks for reading. Many happy total returns.

Published: December 26, 2023

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.