The last few weeks of a calendar year can be exciting. Asset managers chase their benchmarks before the incentive calculator starts anew in January, while pundits are on the lookout for some action that they can call “a Santa Claus rally.” Who knows what other crazy things are in store for us before 2023? (If you do, please write.)

Some coming attractions on The Investment Ecosystem include using the “orgorg chart” to think about the structure of organizations and the ecosystem in general; liquidity and pacing issues; and the proliferation of natural language processing in strategies. Plus, during the first quarter the Academy will introduce a course on communication skills for investment professionals.

On to the carnage readings.

FTX

Normally, the Fortnightly (and this site as a whole) goes for evergreen topics rather than the latest headline material. But given our focus on due diligence (here are links to postings on the topic and to the Academy course about it), the FTX debacle is too important to pass up.

You probably know the outlines of the story, so we’ll offer links to just a few items that frame (another) one for the ages.

On October 27, Bloomberg published an article with the headline “Fidelity Says More Institutional Investors Are Holding Crypto.” Less than three weeks later, one in Institutional Investor asked, “How Did So Much ‘Smart Money’ Get Tangled Up in FTX?” (And there were similar items from every major financial news outlet.)

A lot of big names were involved, although Sequoia, the giant venture capital firm, has taken the biggest PR hit. In late September, it published a glowing profile of FTX founder Sam Bankman-Fried that it had commissioned. A truly astonishing read, which is now available online thanks to internet archiving; Sequoia took it down, replacing that expansive hype with a simple, somber update.

There were a few mea culpas offered (80,000 Hours) from some of the many who had lavishly praised Bankman-Fried, and some well-earned told-ya-sos (such as from Better Markets).

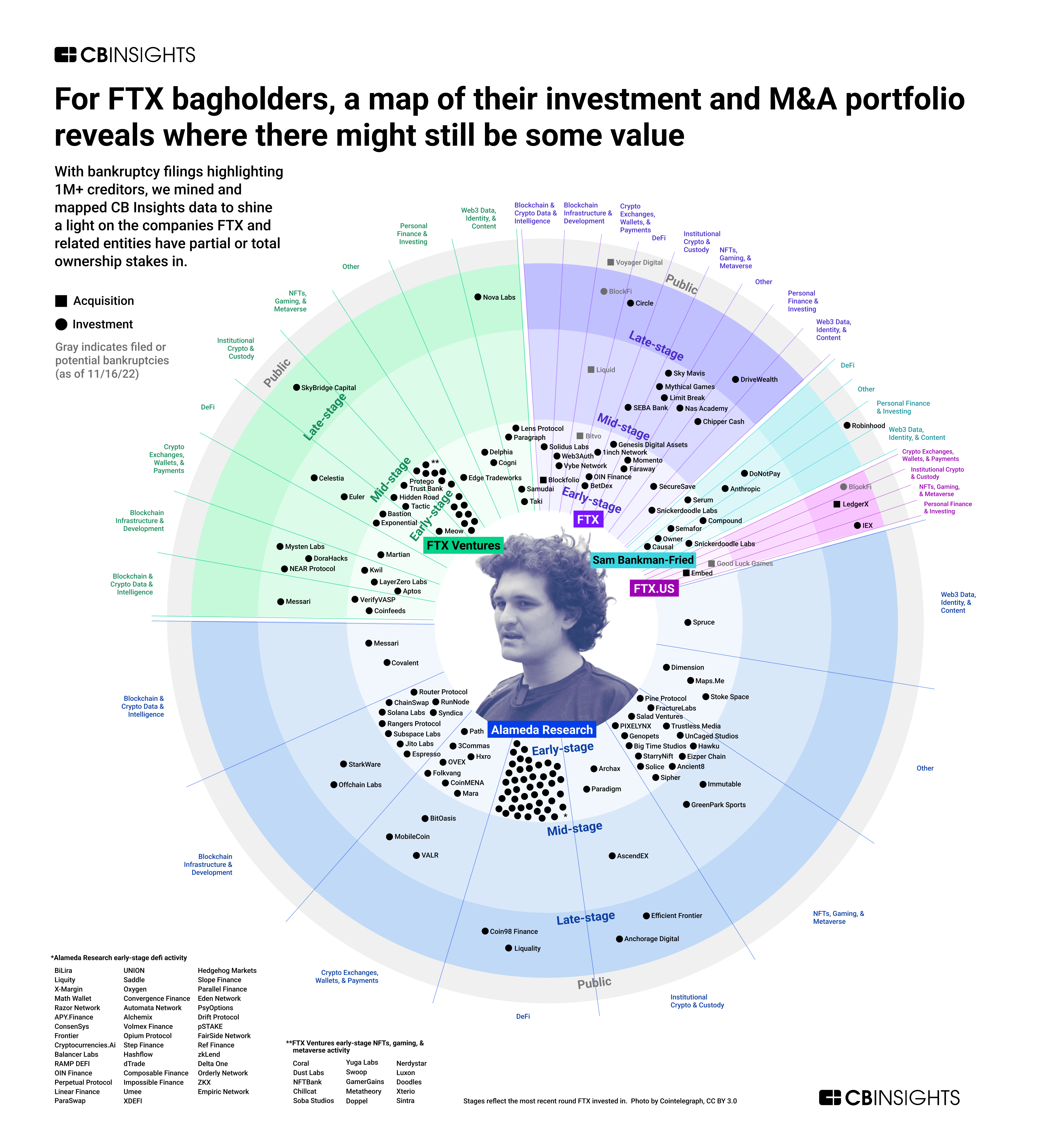

If you want to get into the weeds, check out items from milky eggs and Nansen (although there is much that is not known yet). And, if you’d like to see where a good chunk of the money went, look at the early-stage ring of a CB Insights graphic. Bankman-Fried was so busy betting on the future of crypto that he didn’t see that he was ruining its present.

{kind=link}

An Opalesque webinar with Chris Addy of Castle Hall puts all of it in the context of good operational due diligence. There are a bunch of eye-openers in his presentation. One bullet point: “Blatant conflict of interest when a prop fund also owns an exchange — yet this did not stop investors.”

A reminder from Tyler Cowen: “Many of the real sources of existential risk boil down to hubris and human frailty and imperfections (the humanities remain underrated).”

And, a paragraph to summarize it all, from the incomparable Matt Levine:

I don’t want to minimize the likelihood of intentional fraud and theft. Stuff seems bad. But I want to say that the story of FTX also reads like what would happen if you and a few of your college friends set up a gigantic international financial exchange after like a year or two of working in finance. Oh, your friends are smart. They have decent intuitions about financial stuff; they have good ideas for what products to trade and how to trade them; they can code up a good-looking website. But do they have hard-won expertise, built up over many years, in accounting controls and business processes for running a giant organization? Are they excited about making sure all the paperwork is correct? No, that stuff is boring. Your friends are traders and engineers, not accountants and compliance officers. Also there just aren’t that many of them, and they are running a huge exchange; they are too busy for paperwork. They move fast and break things. They break so many things.

Speaking of breaking things, here were a couple of quotes from different New York Times articles about Twitter published on November 4:

This is a master class in how not to do it. If you were going to rank order ways to upset people, telling them you’re going to do it in advance, without rationale, that is a particularly inhumane way to treat them. (Sandra Sucher, a Harvard professor of management.)

“We are witnessing the real-time destruction of one of the world’s most powerful communications platforms. Unless and until Musk can robustly enforce Twitter’s existing community standards, the platform is not safe for users or for advertisers.” (Nicole Gill, executive director of Accountable Tech.)

That was more than two weeks ago, and it seems to have gotten worse on every front every day since then. Elon Musk has repeatedly miscalculated in matters of strategy and of tactics. Perhaps he can pull a rabbit out of the hat, but at this point in time it looks like he paid an ultra-premium price just to try to kill the social network as fast as he can.

It is worth your time to read Mike Drucker’s “A Rich Man Walks Into a Bar.”

Another hungry mouth

A blog by Bob Veres, “The PE Attack,” covered one of the big topics in the investment advisory realm. At a recent conference:

People were discussing the growing flood of private equity money into the financial planning ecosystem, funding advisory firms that use these dollars to buy other advisory firms at increasingly outrageous multiples, and buying up fintech firms that advisory firms rely on.

Chief among the concerns was the fact that many larger firms are now introducing an additional greedy mouth to feed at their table, beyond the normal stakeholders of the equity owners, staff and clients.

What will the clash between the business of investment advice and profession of financial planning mean for the standards of practice in the industry? The latest chapter in a long-running saga.

Other reads

“Cultures Clash at Salomon Smith Barney,” Rick Bookstaber, Stories.Finance.” Going from a storied partnership to a financial conglomerate; “So, we had this intellectually-driven, collegial, all-of-us-in-the-life-raft-together culture. Then things changed.”

“The Most Important Skill in Finance,” Ben Carlson, A Wealth of Common Sense.

It’s no coincidence that most of the all-time great investors — Benjamin Graham, Warren Buffett, Howard Marks, Peter Lynch, etc. — had the innate ability to explain their investment process in a way that everyone could understand it.

“Persistence of Margins,” Greg Obenshain, Verdad. Margins are historically very high, but “margins and returns on assets are relatively sticky.”

“Private Equity Fund Valuation Management During Fundraising,” Brian Baik, SSRN.

I find that funds managed by low reputation GPs [based on size, age, and performance] show more dramatic forms of NAV inflation by managing upward not only valuation multiples but also portfolio firm earnings.

“Four Structural Differences to Know About the U.K. and U.S. LDI Markets,” Rick Ratkowski, Portfolio for the Future. A concise summary of how the same concept has been implemented in different ways.

“ESG Investment Outcomes, Performance Evaluation, and Attribution,” Stephen Horan, et. al, CFA Institute Research Foundation.

If ESG considerations are to be elevated to an investment objective alongside return and risk, it must differentiate between ESG factors that increase risk-adjusted expected returns and those that do not.

“Longer, Healthier, Happier: Why Working Longer Improves Almost Everything,” Laurence Siegel and Stephen Sexauer, AJO Vista. The United States has a structurally-outmoded retirement system — and one action can address two important problems that “stare each other in the face.”

“Illusions of precision, completeness and control (revisited),” Bob Maynard, Brandes Center. An update of the 2014 paper:

Critics may point to the higher Sharpe Ratios more complex portfolios can generate . . . but Sharpe Ratios are useless in a fat tail/high peak world and, in fact, can drive plan sponsors to create portfolios that seek to pick up proverbial nickels while standing in front of a silently approaching steamroller; greater complexity often makes plans more susceptible to suffering devastating consequences when fat-tailed events roll through.

“Trends in State and Local Pension Funds,” Oliver Giesecke and Joshua Rauh, SSRN. “The reported funding ratio of 82.5% falls to 43.8% under a market-based valuation.”

“Investment Bubbles and Frauds Have a Lot in Common,” Joe Wiggins, Behavioural Investment.

The life of an investment bubble or fraud is predicated on three critical aspects. The story, the performance and the social proof. These operate as a virtuous and vicious circle through the emergence and death of both bubbles and fraud.

“The Rise of 3rd Party Search Firms That Find Consultants,” Dusty Hagedorn, Chief Investment Officer. “Increasingly, asset owners are hiring consultants to find consultants.”

“Fireside Chat with Jim Chanos,” Simplify Asset Management.

I teach a course on the history of financial market fraud, and one of the central tenets in that course is that the fraud cycle follows the financial cycle with a lag. Meaning that the longer the financial cycle or bull market goes on, the more aggressive and the larger the frauds become towards the end of the cycle.

“How Belize Cut Its Debt by Fighting Global Warming,” Anatoly Kurmanaev, New York Times. You’ve heard of green bonds? How about blue bonds?

Ahem

“When you believe in things that you don’t understand, then you suffer.” — Stevie Wonder, “Superstition.”

Inflation and markets

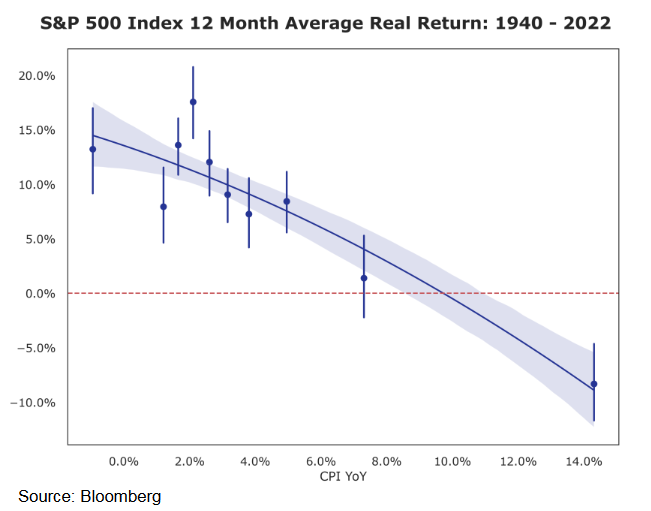

This is from a presentation, “Investing Through A Structurally Inflationary Regime,” by Steve Hou of Bloomberg. It is full of charts like this on equity sectors and factors, other assets, and trading strategies. It also serves as a reminder that we lack sufficient data to make emphatic statements about “what normally happens.”

Postings

You don’t need a paid subscription to read “Talent in the Investment World.” It is a Sampler posting, open to all, that is a compilation of four July perspectives that have an investment take on Talent, a great book from Tyler Cowen and Daniel Gross.

“Creating and Sustaining Process Improvement” looks at the “physics” of change in the investment, operation, and distribution parts of an asset management firm.

All of the content published by The Investment Ecosystem is available in the archives.

Thanks for reading. Many happy total returns.

Published: November 21, 2022

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.