If The Investment Ecosystem is new to you, check out the archives and the recent postings at the bottom of this piece — and please consider a free or paid subscription plan.

A year of change

Looking back a year, the investment landscape was in a completely different state. While gamier areas of the market like SPACs and meme stocks had already been under pressure — and some indexes would continue to rally to new highs at the end of 2021 — last October was a pivot point for many of the growth stalwarts. One by one they started to roll over during the following three months.

Very much alive a year ago, TINA (“there is no alternative” to equities) is now being pronounced dead. (See Morningstar and RIA Advice, for example.)

The U.S. two-year note then yielded 0.4%; it’s now 4.5%, and rates everywhere have risen beyond anyone’s expectations — as has inflation, the driving force behind the moves.

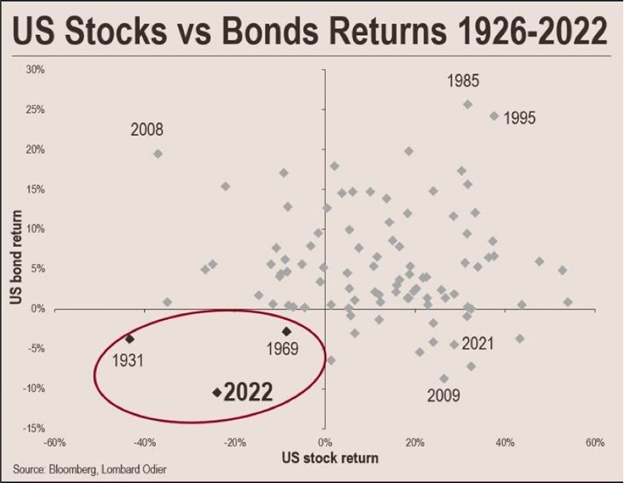

A long list of it-can’t-happen-here beliefs have, indeed, happened here. Most notable are the results for 60/40 and 70/30 asset allocations commonly used by financial advisors on behalf of their clients (and by institutional asset owners as a simple check against their more complex asset mixes), with the component parts ending up in a most unpleasant (and uncommon) cominbation.

{kind=link}

Last October also marked the pivot for ESG. Up until then it was a juggernaut, but the debate has changed and the previously-strong adoption indicators have been flattening out. (Interestingly, there was a budding interest in many ESG-like topics in advance of the financial crisis, before that diminished as other concerns took precedence. That could be a factor now too.)

Private strategies — the most red-hot of the red hots — have not been marked down anywhere close to similar public exposures, even though the anecdotal evidence would indicate that the cuts are coming. The fondness for the structural attractiveness of lagged pricing may turn into something else. Already, the denominator effect is causing problems (that impact on some asset owners was outlined in an August piece from Nasdaq).

The ripple effects of all of this are spreading throughout the system, as should be expected given the length of the previous trends and the special power of interest rates to affect the pricing of assets and the availability of funding. Youngsters are even seeking advice from their elders; Rich Handler and Brian Friedman of Jefferies have responded with “A ‘Boomer’s Guide’ to Dealing with an Increasing Interest Rate Environment.”

The new dynamics

In a report, “The New Dynamics of Private Markets,” PGIM asserts that “neither the pandemic nor the subsequent inflationary shocks appear to have significantly dampened [the] momentum” that has been intensifying for the last few decades in that realm. Regarding private credit, banks and finance companies have abandoned many forms of lending, opening up opportunities, and investors are still clamoring for yield. Bolstering private equity, “a growing number of business models may be better suited for private markets,” and companies are choosing to stay private longer than they have before.

In addition to examining each of those areas, the implications for asset owner portfolios are covered. Included are the need for “more flexible investment approaches given blurring across publics and privates” and “a more sophisticated understanding of liquidity risk,” plus the effects of growing ESG-related offerings.

Many of the forces that are mentioned have been in place for a while. As such, in the light of future Octobers, the report may be seen either as a wise recommendation to stay the course or a too-optimistic marker on the path to more difficult times.

Trust

Chestnut Advisory Group has published “Trust for the Win,” in which it argues, “Trust is the leading factor behind an investor’s decision to hire an asset manager.” The piece begins with the top five factors that drive selection. Not included is performance, which should be number one, since hiring is almost always conditioned upon a manager meeting a past performance hurdle.

That aside, Chestnut presents a matrix using the variables of warmth and competence to consider the nature of trust; it believes that “no amount of competence can compensate for a lack of warmth.” Competence (primarily as judged in performance) without warmth can become suspect:

At worst, investors fear that extremely competent managers may use their skills to benefit themselves at the expense of clients. The classic example of this fear is the worry that a successful manager will not close a winning product when it reaches capacity, but will instead become a dreaded “asset gatherer,” maximizing AUM — and the manager’s income — while diluting the investment returns of their entire client base.

Some dos and don’ts are included for asset managers wanting to up their trust game.

The survival game

Speaking of asset management, Joe Wiggins thinks that the cultural environment for fund managers leads to poor incentives and mediocre performance:

There is a major incentive problem at the heart of the asset management industry, where the interests of clients and the professional investors who run money for them are often poorly aligned.

The development of this type of incentive structure means that the active fund management industry has evolved to a point where making high conviction, long-term decisions is irrational behaviour for many participants. Even though it should be one of its primary purposes.

Other reads

“Hedge funds: The industry strikes back,” WTW. A look at a few positives and, despite the title, some negatives too, including:

While we welcome regulations in Europe and Australia focusing more on costs and expenses, we still witness resistance from the asset management community. More worryingly, we have started to see some upward pressure from hedge funds on fees, and there is growing diffusion of a fee structure in the industry that we are very concerned about: hedge funds that are set-up as expense pass-through platforms.

“Predicting Growth,” Greg Obenshain and Brian Chingono, Verdad. Third in a series on predicting earnings growth; “The data shows that we need to be very humble when plugging a terminal growth assumption into a discounted cash flow model.”

Ashby Monk tweet:

ESG ratings purport to work like credit ratings, and condense all ESG factors down into one convenient value. With credit ratings, the value of the rating is that it can usually be linked to probability of default. But with ESG ratings, the analogous probability would be . . . what?

“Passive Investing, Mutual Fund Skill, and Market Efficiency,” Da Huang, SSRN. “In this paper, I show the rise of passive investing is a reason for, rather than an anomalous outcome of, a more skilled mutual fund industry.”

“A marketing conundrum,” Mark Schoeff, InvestmentNews. The print cover of the magazine characterized the story in this way: “Creativity and Compliance: New SEC regulations give advisers the freedom to advertise, as long as they follow 430 pages of rules.”

“Where Do the Golden State Warriors Go From Here?” The Daily Coach. Beyond the specifics regarding recent incidents, this includes the age-old investment organization question:

Is keeping talent more important than maintaining culture?

“Opportunities in Small Caps,” Thomas Garrett, Verus. The small cap premium may be gone (or maybe it’s just been hiding), but that shouldn’t obscure the greater possibilities for active management within the category than those found elsewhere.

“Top 5 considerations for asset managers as we head into budgeting season,” Mike Carrodus, Substantive Research.

The SEC has ensured that regulatory complications in this market are back with a vengeance. By announcing that they would not extend the no action relief that allows European asset managers to pay American brokers for research in cash, the SEC has created a massive headache for both the buy and the sell side.

“From Epsilon to Omega: Making Small Strides Toward Important Goals,” Matt Greenwood, Two Sigma. A glimpse of some “inside language” of the firm — and the important concepts behind it.

“Leverage in Private Equity Real Estate,” Jacob Sagi and Zipei Zhu, SSRN.

With PERE, existing work provides mixed or little evidence that leverage is used to amplify skill and consistently hints that its use shifts the balance of benefits towards fund sponsors over their limited partners.

“Refresher Readings,” CFA Institute. Available to members of CFA Institute, this includes a large number of 2023 updates to a wide variety of topics, as well as those from 2022.

A foundational principle

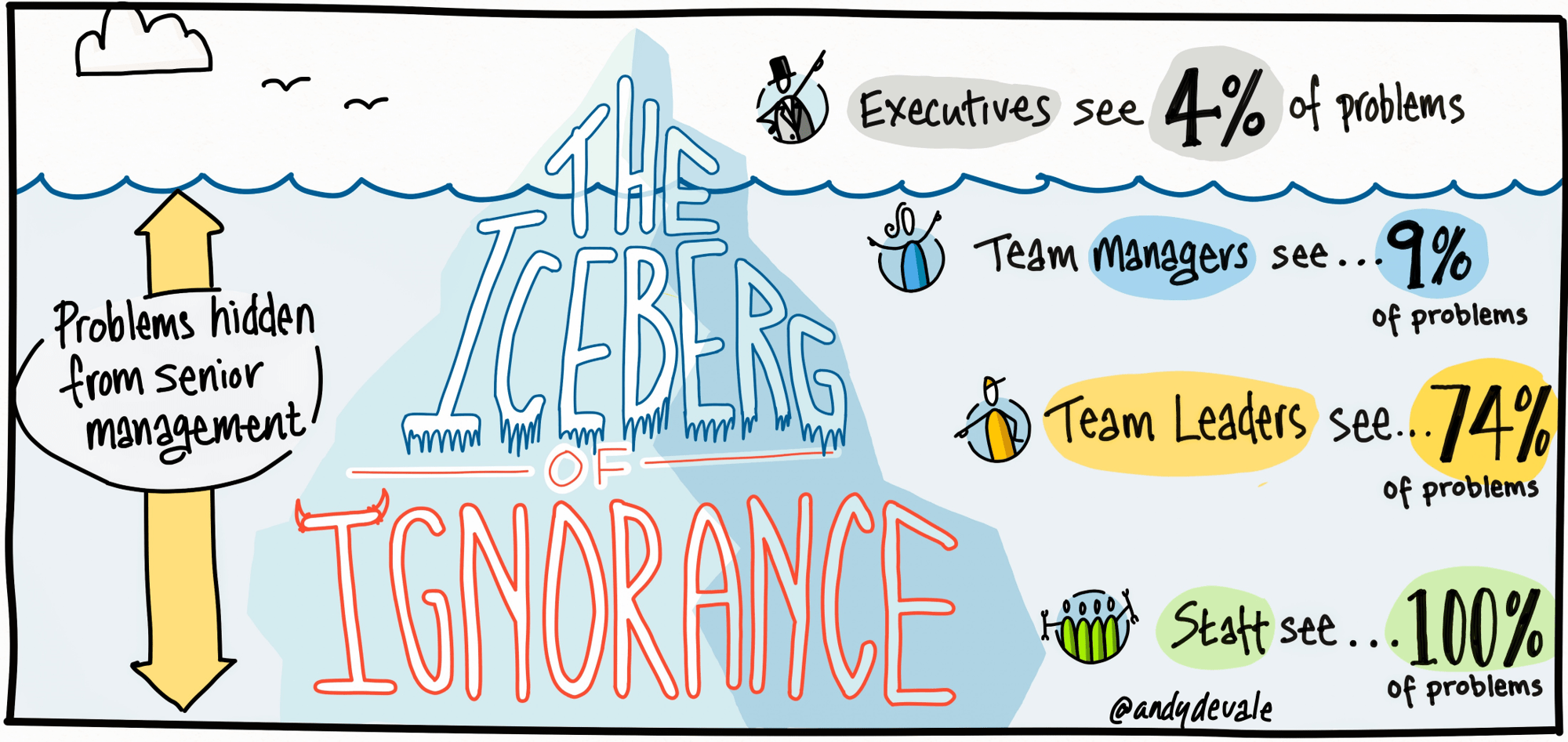

A posting by Paul Taylor, “Few People Get Promoted For Asking Difficult Questions,” addresses how organizations identify and attack problems. The image below comes from a section titled “What Is An Expert Anyway?”

While the principle is illustrated in regards to hierarchies of staff, teams, and executives, it is broadly applicable in the investment world too, even where there are flatter org charts. Despite the reality depicted, we often cling to “quite a narrow view of expertise,” relying on things like “position in the hierarchy, titles and years of service” as indicators of importance and insight.

For example, when doing due diligence, the most time and energy is usually spent with a small number of “key” people, but those highest up in an organization are skilled at promoting the narrative of how things are done. To see how things are really done — and to try to uncover the messiness not addressed in that narrative — it pays to do the opposite. You need to get below the water line to view the rest of the iceberg.

Speaking of due diligence

“Cynicism is attributing the worst motives to people. Skepticism is looking for the truth.” — Penn Jillette.

Postings

The four-part series on Bill Gross and Pimco, published for paid subscribers in May and June, is now available to all in a compilation posting. It is a broad look at lessons for asset managers — and for those who evaluate them and invest with them.

Two new essays:

“Looking in the Rearview Mirror.” We’ve seen the progression before: Unexpected market moves leading to a blow-up and then a reexamination. What’s really needed is a new approach to risk management.

“Revaluation Alpha and Selection Practices.” Among the challenges for those evaluating investment strategies and managers is not being fooled by changes in relative valuation that may be transitory.

All of the content published by The Investment Ecosystem is available in the archives. If you explore the categories of interest to you, you are sure to find some ideas that you can put to work now.

Thanks for reading. Many happy total returns.

Published: October 24, 2022

Subscribe

To comment, please send an email to editor@investmentecosystem.com. Comments are for the editor and are not viewable by readers.